Why I Keep Buying Industrial REITs

Industrial REITs are great. They offer several appealing factors:

- Evidence of strong growth.

- Material mark-to-market opportunities are still present on existing leases.

- Structural tailwinds over the next decade.

- Opportunities to create additional value with redevelopment projects.

But the market doesn’t like industrial REITs today. Market implied cap rates on industrial REITs plunged. Industrial REITs used to trade at premiums to NAV (Net Asset Value). Now we see material discounts.

Due to stronger growth in AFFO per share, industrial REITs also achieved higher AFFO, Core FFO, and FFO multiples than other property types. Those premium multiples have largely disappeared. That’s remarkable.

We own three industrial REITs:

We’re going to talk about them, but I’m also going to include Digital Realty (DLR) in some charts so investors can see what an overrated REIT looks like.

The Layout

I’ll make the case chronologically. It may seem strange to emphasize what already happened, but it is important. Strong companies typically deliver growth in most years. A consistent history of growth demonstrates a functioning business.

Growth Per Share Matters Most

Many equity REITs regularly issue equity to fund acquisitions. That’s fine. The company will have more shares outstanding and more real estate. Some REITs create value by issuing equity to fund acquisitions. Others destroy value. Industrial REITs have used this technique to enhance value.

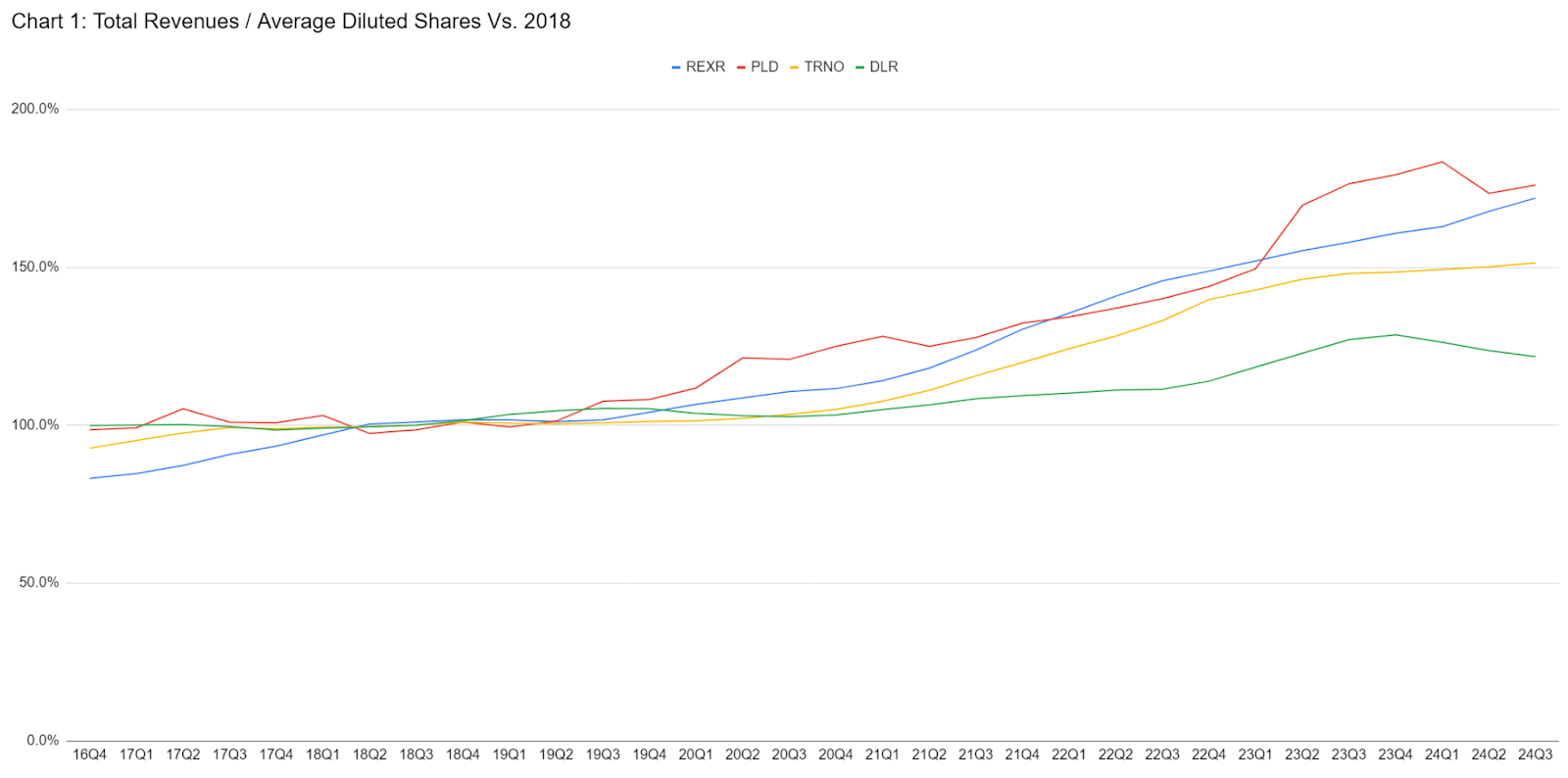

Industrial REITs Grow Revenue Per Share

You’re probably familiar with metrics like “Earnings Per Share” or “EPS”.

For equity REITs, we focus on metrics such as AFFO (Adjusted Funds from Operations), Core FFO (Funds from Operations), and FFO. However, to really understand a REIT, you should look at more of the financial statements. It helps to identify trends. For instance, you can look at revenue per share over time. It’s much easier to grow AFFO per share when revenue per share is growing.

To make it easier to compare several REITs, we need to normalize values. One way to do that is to just normalize based on a single year. I used 2018 to standardize my charts.

Here’s a chart comparing the four REITs:

Which one looks bad? DLR.

It’s not a trick. As we go through these charts it’ll be pretty obvious that the only area where industrial REITs are underperforming is the share price. On fundamental metrics, industrial REITs remain among the best sectors.

Just a quick note about Prologis. You’re going to see that bump in the red line in each chart. PLD includes a development business. The recognition of revenue and gains in that business is extremely lumpy. They recognized an enormous value in Q2 2023. The charts use the trailing four quarters. Q2 2024 and Q3 2024 don’t have that extra revenue in the trailing four quarters.

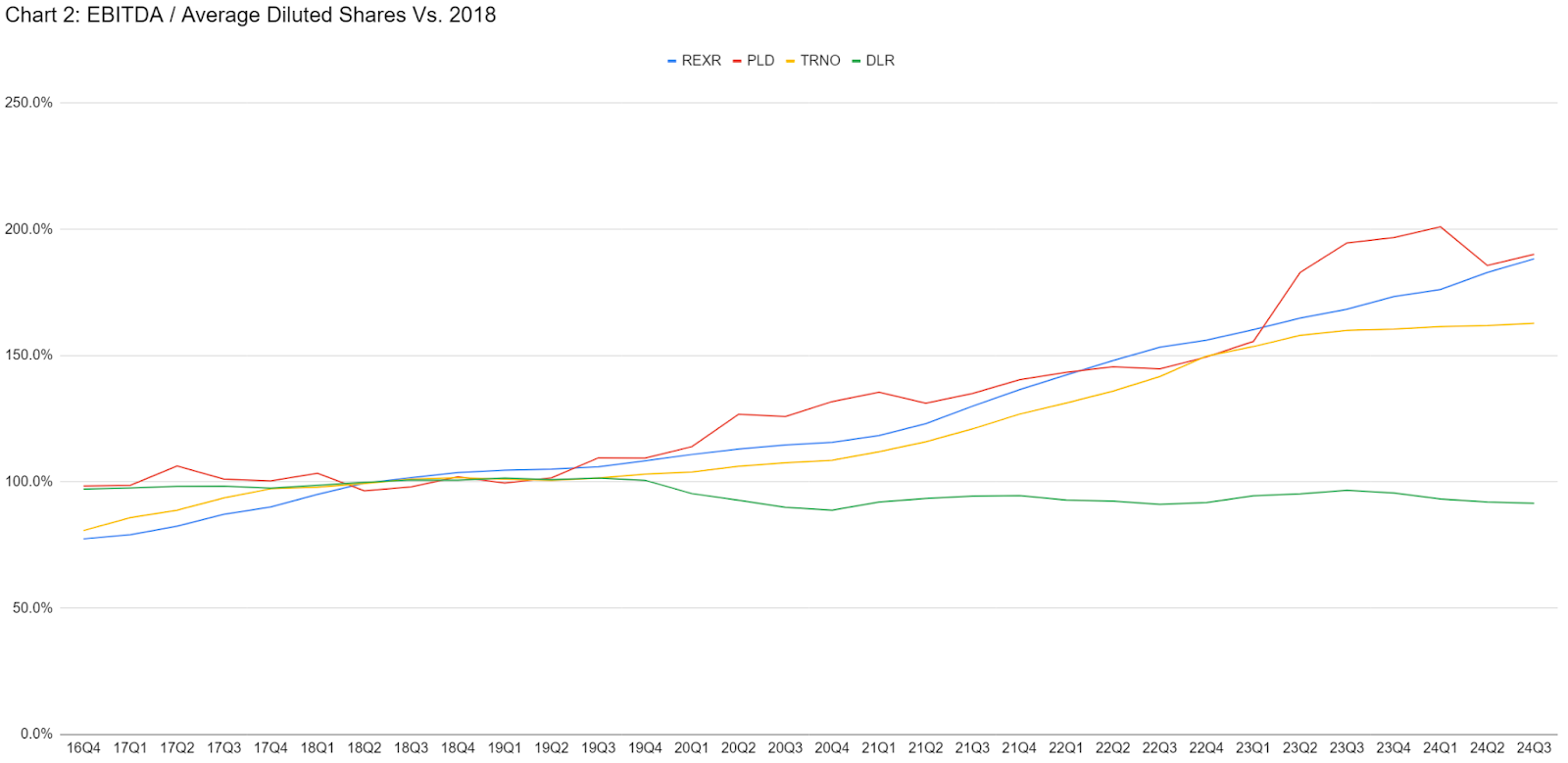

EBITDA Per Share

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is another important metric for REITs. Since income taxes are typically extremely low for REITs (immune to most income taxes), EBITDA (normalized for any strange events) serves as a rough approximation of the amount available to be split between bondholders and shareholders. Assuming the REIT maintains similar margins, EBITDA per share and revenue per share will probably have pretty similar growth rates.

How about we check out that chart?

Wow, look at that. Somehow DLR saw EBITDA per share decline while it increased substantially for our three industrial REITs.

How did that happen? It all comes down to EBITDA margins.

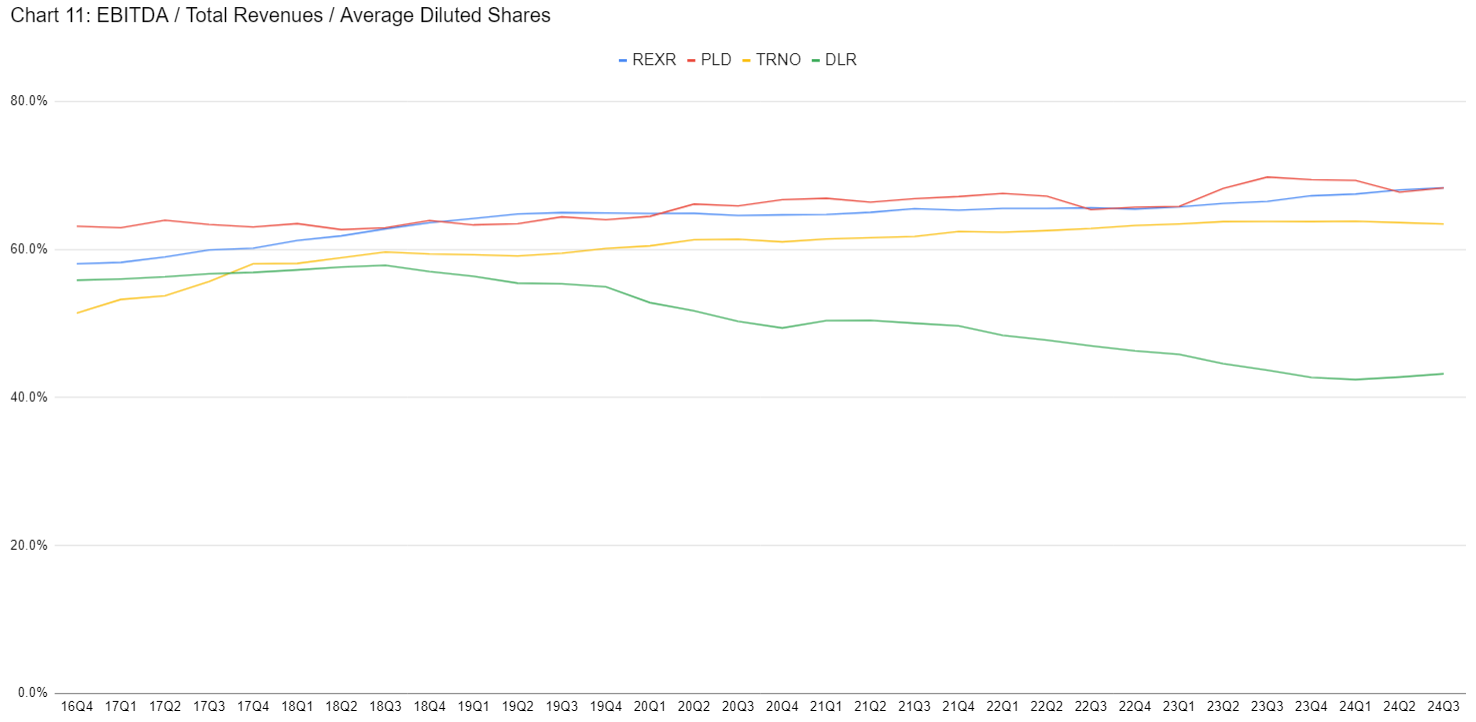

EBITDA Margins

We can see that EBITDA margins for the industrial REITs were improving while EBITDA margins for DLR were getting worse.

As a shareholder, you want to see margins improving. All 3 industrial REITs were able to improve margins. PLD started with the best margins, but REXR landed at a similar rate to them. TRNO started with the weakest margins, but they improved significantly.

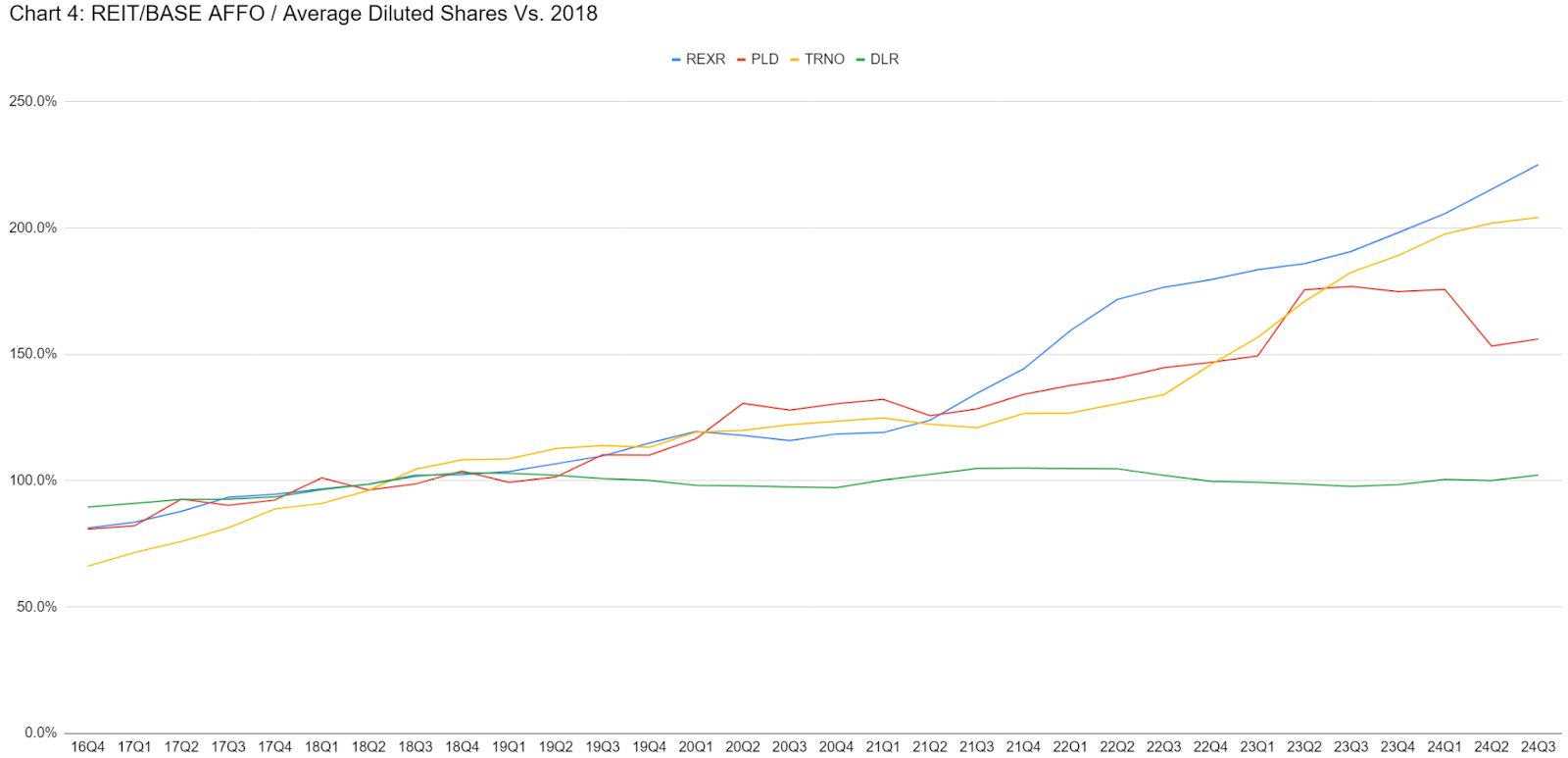

AFFO Per Share

We know which REITs were able to grow revenue and EBITDA, but which ones were able to grow AFFO per share? Yeah, you guessed it.

I’m using “REIT/BASE AFFO”. That’s because REIT/BASE came up with a way to calculate AFFO that achieved my stamp of approval for handling adjustments correctly. It makes numbers more comparable between REITs by eliminating low-quality adjustments to create an even playing field. All of the industrial REITs delivered excellent growth. DLR is the pathetic line, again.