SBAC Q3 2024 Update: Strong Quarter for SBA Communications

Summary

- AFFO attributable to SBA Communications in line with estimates.

- Full-year guidance was raised by about 0.53%.

- SBA Communications announced the acquisition of 7,000 sites in Central America from Millicom.

- The transaction carries a cash cap rate of 9.13% If we assign overhead and use EBITDA, it should be about an 8.72% yield or an 11.5x multiple.

- No shares repurchased during the quarter, which is fine since SBAC was pursuing the acquisition instead. The acquisition should be accretive as soon as it closes in 2025. It also gives SBA Communications greater leverage within the market.

SBA Communications (SBAC) delivered a solid Q3 2024 earnings report. Share prices went down the following day, but that may have been driven partially by American Tower (AMT) having a weaker report and dragging the sector lower.

Results for AFFO Attributable to SBA Communications Per Share

- AFFO consensus estimate: $3.31

- AFFO attributable to SBA Communications Per Share Result: $3.31

- Result: Matches estimate.

Note: Some headlines compared AFFO per share of $3.32 (not attributable to SBAC) with consensus FFO estimates of $3.20. Consequently, those headlines incorrectly declared SBA Communications beat estimates by $.12 per share.

Guidance for AFFO

- Old Guidance for AFFO: $13.06 to $13.43. Midpoint $13.245.

- New Guidance for AFFO: $13.20 to $13.45. Midpoint $13.325.

- Change: Up $.08 or 0.60%.

Guidance for AFFO Attributable to SBAC

- Old Guidance for AFFO attributable to SBAC: $13.01 to $13.38. Midpoint $13.195.

- New Guidance for AFFO attributable to SBAC: $13.14 to $13.39. Midpoint $13.265.

- Change: Up $.07 or 0.53%.

- Consensus estimate was $13.19. New guidance midpoint is $.075 higher than the prior consensus estimate.

Note: AFFO Guidance is a bit more complex because we have to adjust for AFFO attributable to SBAC. I’ve taken care of that in the tables above. The line I want investors to notice for guidance is shown in bold.

5 Key Questions

I’m interested primarily in 5 things for this report:

- Was SBA Communications repurchasing shares?

- Were there any acquisitions?

- What is the change in guidance?

- What is the reason for the change in guidance?

- Any other signals about the industry beyond current-year impacts?

Did SBA Communications Repurchase Shares?

No shares were repurchased during Q3 2024.

The most recent repurchasing activity was in April 2024 at $213.30 per share.

Acquisitions

The big announcement was that SBA Communications reached a deal to purchase sites from Millicom. I’ve compiled and organized information from the earnings release and earnings call here. This is a sale-leaseback transaction.

- Timeline: SBA Communications will close the deal some time in 2025.

- Sites: 7,000

- Type of site: About 90% tower, 10% to 12% rooftop.

- Price: $975 million.

- Projected revenue: $129 million.

- Projected cash flow: $89 million.

- Forward cash flow multiple before overhead: 10.96x

- Forward cash cap rate: 9.13%

- Projected overhead (from call) $3 to $5 million

- EBITDA contribution based on overhead: $84 to $86 million.

- EBITDA multiple at midpoint: 11.47x.

- EBITDA yield: 8.72%

- Lease structured in USD (United States Dollars) so no material currency fluctuations.

These figures are based only on the tenants currently present.

Other key factors:

- Millicom enters into country-specific MLAs (Master Lease Agreements) with SBA Communications. Millicom will lease all sites for an initial term of 15 years.

- All 1,500 sites SBA Communications was already leasing to Millicom are extended for a new 15-year term.

- For 7 years SBAC will have exclusive rights to build up to 2,500 build-to-suit sites in Central America for Millicom. These sites would have an initial lease-term of 15 years.

- Currently the tenancy ratio (average tenants per site) is 1.2. If there were no other tenants, the ratio 1.0. The other 0.2 comes from other tenants Millicom was able to sign.

- SBA Communications expects to increase the tenancy ratio, which would enhance the revenue and cash flow. If it increases substantially, Millicom would be able to share in the benefits.

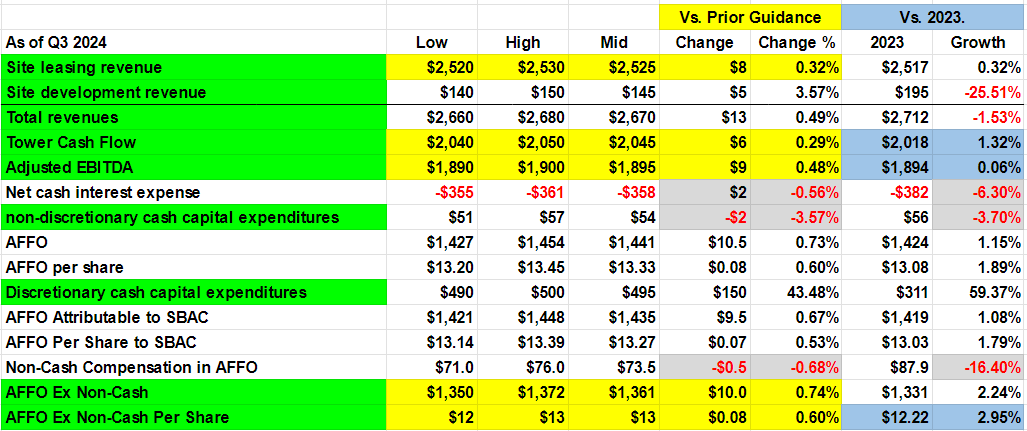

Change in Annual Guidance for SBA Communications

For AFFO, I prefer to focus on the very bottom value: “AFFO ex-Non-Cash Per Share”.

You can see the update, and the year-over-year growth, in the table below:

Source: The REIT Forum

Color coding:

- Bright green (on the name in the far left) indicates the figures we look at closer.

- Yellow highlights the current guidance and change vs. prior guidance for those values.

- The blue highlights comparison to 2023.

- The gray values represent figures that may show up as negative, but are actually positive developments.

Note: It suddenly became clear to me that I could probably enhance the presentation for readers. I’ll think about ways to do that. If you have some ideas, hit the button at the top to “view in browser” and provide a suggestion in the comments section.

That’s a solid report for SBA Communications. Our preferred AFFO metric saw guidance increase by $.08. About $.02 of that impact comes from foreign exchange rates. Holding foreign exchange constant (compared to Q2 2024 guidance), it would be an increase of $.06 (up 0.48%).

SBA Communications Enjoyed More Revenue

Revenue growth was a little bit better than expected including a little more site development revenue than previously expected.

There was also a tiny dip in projected interest expense. However, the biggest factor was simply increasing revenue. The big acquisition is expected to close in 2025. It is not driving the change.

Notes on SBA Communications’ Earnings Call

Positive commentary.

Still within normal leverage range. Net debt to annualized adjusted EBITDA will move a bit higher following the acquisition.

The Millicom deal should not require any additional capital expenditures initially. Any increase would be the typical capital expenditures with signing another tenant. The return on that kind of capital expenditure is very attractive.

The acquisition should be immediately accretive to all metrics. That should make sense intuitively given the relatively high cash flow yield and EBITDA yield. Towers in Central America typically trade at much higher cap rates than those in the United States, so those acquisitions should usually be immediately accretive.

It seems SBA Communications is leaning towards mostly rolling over debt, rather than paying down debt. Per the earnings call, management would prefer acquisitions or repurchasing shares to debt reduction.

SBA Communications expects to sell some assets in the Philippines. They entered it as a potential growth market, but the cell carriers remained highly fragmented and SBAC hasn’t been able to achieve scale in the market at a reasonable valuation. Consequently, they don’t see it enhancing results compared to focusing on the markets where they have a stronger presence and at least one major tenant.

Their acquisition is improving their presence in 4 countries and starting their presence in one other country. However, the operator they are working with is one of the major players. That gives them a much better position for scaling operations in those markets.

Note: The acquisition from Millicom may be referred to as “Tigo” due to the structure Millicom used for holding the assets.

Previewing Target Adjustments for SBA Communications

We previously reaffirmed targets on 7/30/2024. They are due for another update. However, American Tower also reported. I want to give that a more thorough review before I settle in on the adjustments for SBA Communications.

Increased guidance for AFFO per share is great. However, the interest rate environment is awful:

Source: MBS Live

I highlighted July 30th, 2024, on the chart since that was when we previously reaffirmed targets. As you can see, rates plunged in the subsequent 45 days. If this update was coming in the middle of September, it would definitely push targets higher since we would have lower rates and higher guidance.

However, this update is coming in late October. Based on the swing in interest rates over the last 40 days, most equity REIT target adjustments will probably be negative. This is a good quarterly report for SBA Communications, but it probably won't be enough to overcome the swing in interest rates.

No change to thesis, risk ratings, or targets yet. In the subsequent update, there will probably be a small negative adjustment to targets, but no change to thesis or risk rating. I do not plan to buy or sell shares in the immediate future, as SBAC is already our largest non-cash position.

Disclosure: Long SBAC, AMT

Member discussion