Realty Income Q3 2024 Earnings Update (Includes Bonus Section)

Summary

- AFFO per share is the most important metric. Guidance increased slightly. Matches consensus forecast for the year. Quarterly AFFO per share beat by $.01.

- The tiny increase in guidance may be influenced by a bump in the projected acquisition volume for the year.

- Net lease REITs like Realty Income have done surprisingly well for a period of rising interest rates. Sometimes we see strong correlation to Treasuries, but sometimes we do not.

- Bonus section not suitable for Seeking Alpha at the end.

Article Starts

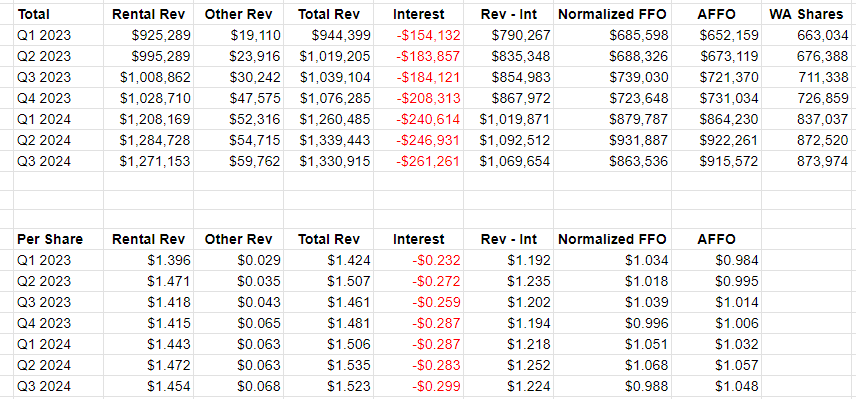

Q3 2024 was a respectable quarter for Realty Income (O).

Normalized FFO per share for the quarter came in low. Doesn’t matter because nearly the entire miss came from a single non-recurring item. Normalized FFO doesn’t strip out every possible non-recurring item. It is better than regular “FFO”, but it doesn’t catch everything. Consequently, normalized FFO came in at $.99. If we adjust for the non-recurring item, it would be $1.061. That’s pretty close to the consensus estimate for $1.07.

Looking at AFFO per share, we see $1.05 beating the consensus estimate of $1.04.

For Realty Income, AFFO per share is usually the most important metric.

Guidance

Once again, we see a slight boost to AFFO per share guidance paired with an increase in net investment volume. Acquisitions are an important lever for Realty Income to drive growth in AFFO per share over time.

Here’s the guidance update with my notes:

Guidance for net acquisitions (or net investments) is up $375 million.

AFFO per share guidance is up slightly. Midpoint is $4.19. That matches the consensus estimate.

Issuing Shares

During the quarter Realty Income raised another $271 million from selling shares at a weighted-average price of $62.25 per share.

That price is high enough to fund accretive investments, which is how Realty Income enhances growth in AFFO per share.

I use the following table to help investors make sense of the equity issuance:

Investors who don’t understand REITs would complain about Realty Income issuing shares. They would argue that the REIT should simply raise revenues. That doesn’t work. Realty Income is leasing properties out for decades at a very stable rate. They have some modest rental rate increases built into leases, but they can’t just raise rents on a tenant with a lease.

However, when Realty Income trades at a high enough share price, they can issue new equity and use it to fund acquisitions. This is the secret sauce for net lease REITs. Other REITs can use it also, but it’s a bigger part of the equation for net lease REITs.

This post is available to anyone who is a member of our service. Even free members have access. However, we need signups to keep the the site from getting scraped.