Portfolio Update - December: Time for Macro Charts

- Interest rates were pretty strange. Climbed hard, then plunged.

- My cash allocation continued to increase in November. It is now about 24.5%.

- Politics are driving perceptions about the economy. Earnings grow regardless of whether team red or team blue has the White House.

- Earnings forecasts call for material growth in revenue and a substantial increase in profits. We’ve got some nice charts.

- I’ll cover potential upcoming trades in the section for paid members. The rest of the article is available to everyone.

Interest Rates

Treasury rates are actually down over the last month. That feels pretty insane after how much they increased up until the final week of November.

To help readers isolate the last month and the last week, I’ve marked three dates in the charts:

- One month ago is highlighted by the vertical bar with the little symbols.

- One week ago is highlighted by a blue circle.

- The end of November is highlighted by the white circle.

Obviously, the end of November is also the end of the chart, but the sharp move can make it a bit harder to see precisely where it ends.

We start with the 2-year Treasury:

Source: MBSLive

The 2-year rate is down about 6.5 basis points (0.065%) on the month.

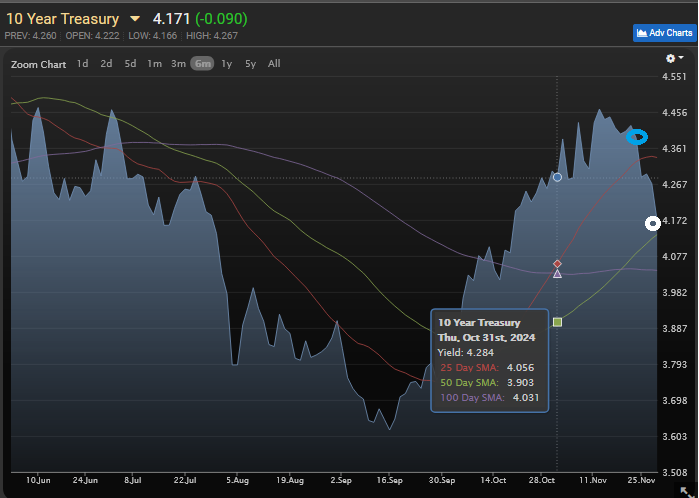

Next, we have the 10-year Treasury:

Source: MBSLive

The 10-year rate is down 11 basis points on the month.

That should be favorable for our investments since the valuation can be sensitive to interest rates.

However, investors should remember that Treasury rates are still up substantially relative to the end of September. We had a dip in November thanks to the final week, but it wasn’t enough to offset the huge increase in yields we saw during October. Treasury prices are still down over the last two months. However, the iShares Preferred and Income Securities ETF (PFF) still managed to squeak out a positive return over that 2-month period. Seems wild given the interest rate sensitivity, but credit spreads remain very low.

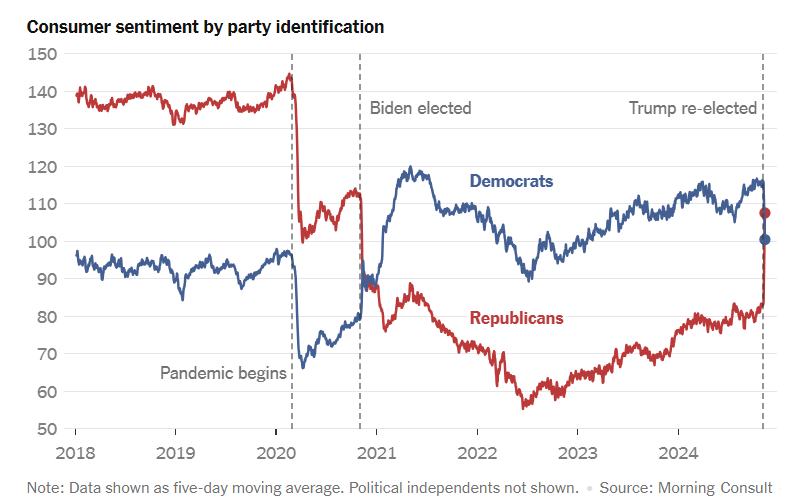

Before touching on my macro views, I want to highlight the absurdity of how most people look at the economy.

In the United States, respondents to economic surveys (also known as “consumer sentiment”) overwhelmingly base their view on the most recent presidential election. I don’t do that, because it’s stupid.

Here’s a chart to demonstrate:

Source: Morning Consult

That chart really demonstrates the “my team good, other team bad” mentality.

Unlike most respondents, my expectations for the macro economy are not changed substantially by who controls the White House.

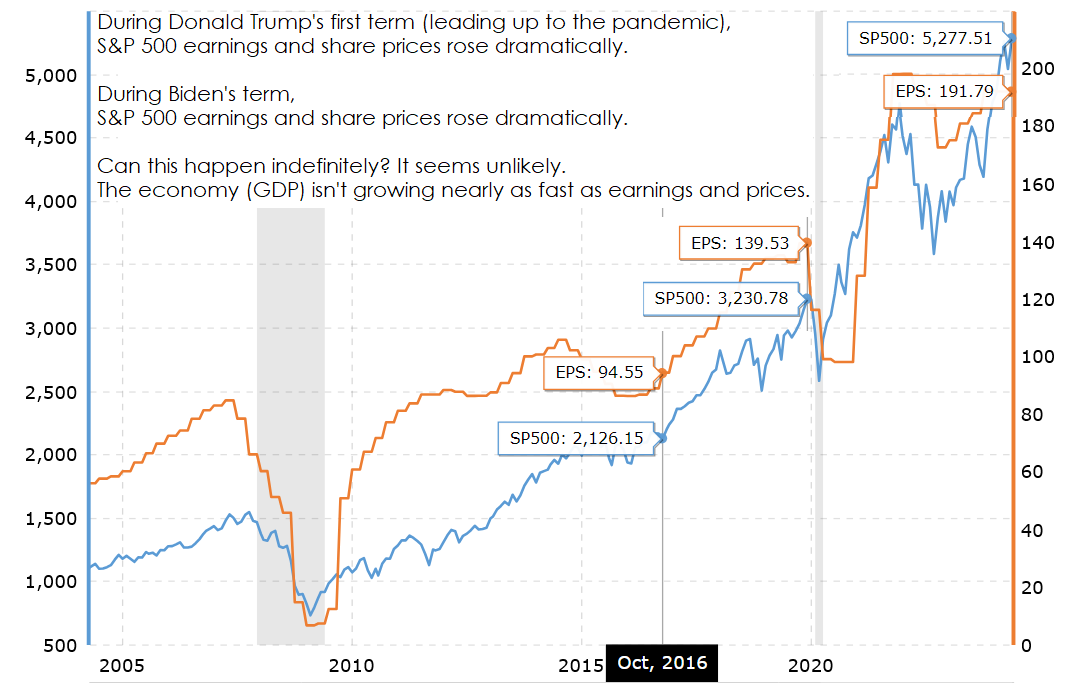

Earnings and prices have gone up regardless of which party controls the White House.

Source: Macrotrends

Note 1: The second measurement date is set to December 2019 to remove the impact of the pandemic.

For a bit of perspective, since October 2016, earnings per share for the S&P 500 doubled (up 103.8%) within the chart. However, that chart cuts out in May 2024. The S&P rallied significantly since then and earnings projections continued to increase dramatically. Consensus estimates for S&P 500 earnings suggest strong earnings growth again in 2025.

Data Quality Disclosure: Data may not be entirely accurate. It’s remarkable how much sources disagree on something as simple as the S&P 500 earnings per share. Fact Set should be a more reliable source and I will use them below.

I want to share a few more earnings projections charts. I proactively apologize for the resolution here. FactSet uses PDFs and doesn’t have them scaled for high resolution. I don’t know how that is still a thing in 2024, but it is.

A Moment to Gripe

FactSet is one of the huge data companies. They can afford to do better when producing these reports.

These PDFs are:

- About 820 pixels wide.

- About 673 pixels wide if we exclude the utterly pointless white margins.

- Don’t zoom well because that’s the actual file size.

It would be possible to store a much better image and just let the user adjust it by zooming.

For perspective on pixels:

- An iPhone 13 has a width of 1170 pixels (73.8% wider than the charts).

- A Samsung S24 has a width of 1080 pixels (60.5% wider than the charts).

Therefore, they could provide a dramatically less pixelated chart even if they assumed:

- The reader was on a phone.

- The reader didn’t know how to spread their fingers on the screen to zoom in on a chart.

I’m constantly blown away by companies intentionally making their product look worse.

Back To Analysis

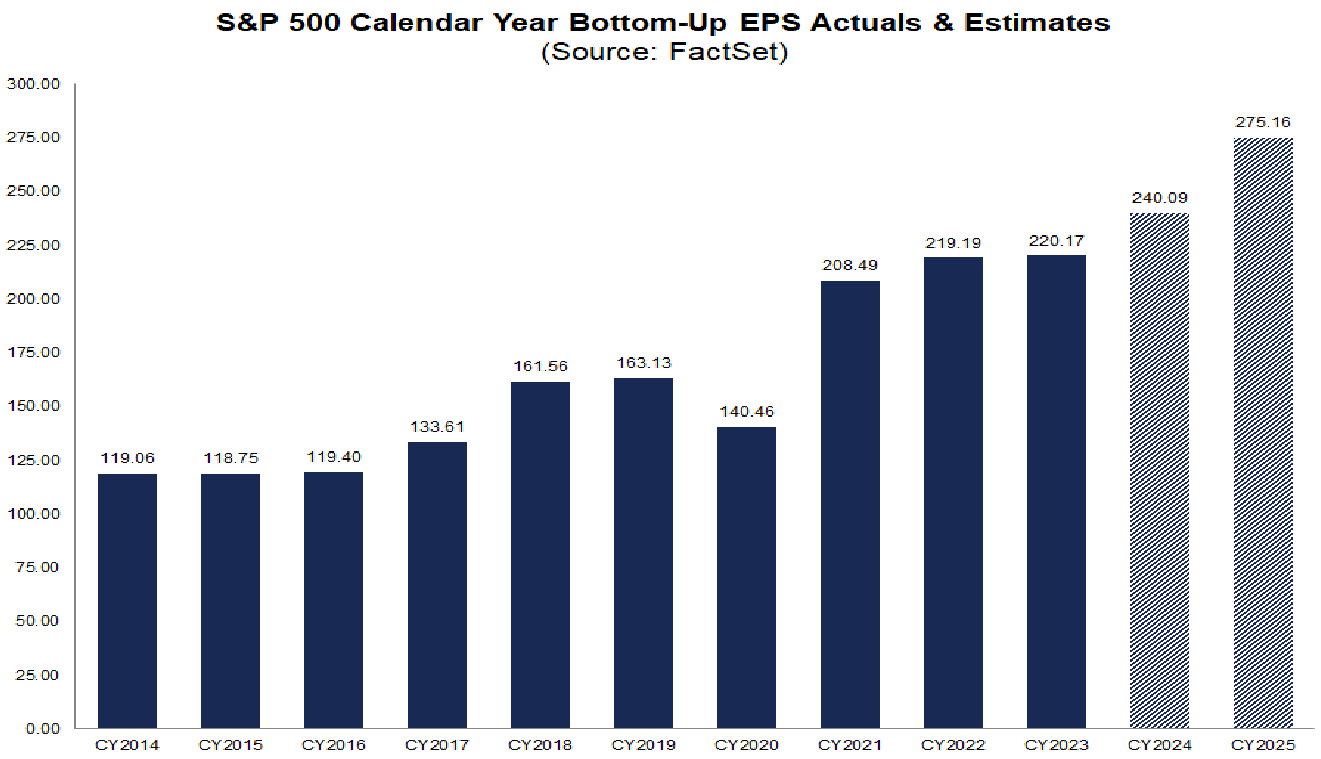

These are the annual EPS results and forward estimates:

If 2024 plays out according to projections, then earnings will have doubled from 2016 to 2024. Meanwhile, earnings growth is expected to be strong again in 2025.

Note: Far be it from me to correct someone on math, but the report also says analysts are forecasting earnings growth of 15.0%. I can do elementary math. $275.16/240.09 = 1.14607. That rounds to 15%, but it doesn’t round to 15.0%. Don’t add a decimal just to abuse it.

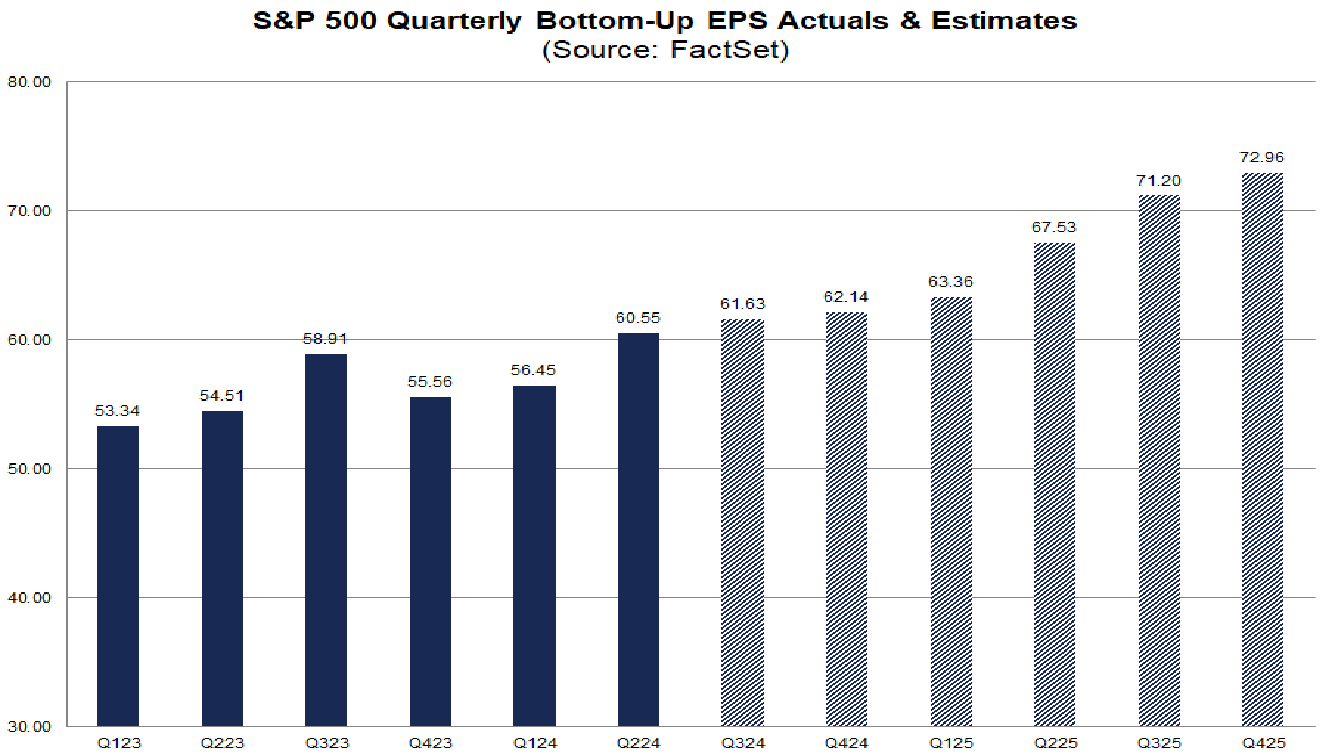

If we look at the individual quarters, we can see that the projections are really picking up some steam around Q2 2025:

Will that all happen?

Who knows.

I’m highlighting the earnings because it’s relevant to the broader economic environment. The multiples on the S&P 500 are much higher than on REITs. That makes sense in the perspective of extremely strong growth in earnings. But how long can the entire S&P 500 grow earnings at this rate?

Can I say something that will bother some people? Of course, that’s my job.

Let’s break it down by year:

- 2014 to 2016: Earnings were relatively flat.

- 2017: Pretty strong growth. Earnings up 11.9%.

- 2018: Earnings surge. It’s the first year of the tax cuts. Earnings up 20.9%. You might even think companies were manipulating their accounting to push profits into 2018.

- 2019: Earnings growth drops back to almost nothing. Earnings up 0.9%. The lack of growth this year supports the idea that 2018 included some 2017 profits.

- 2020: Pandemic drives huge deficit, but accounting negatively impacts earnings.

- 2021: Massive deficit continues. Earnings surge relative to 2019. Earnings up 27.8% over 2 years.

- 2022: Deficit plunges. Still huge, but vastly lower. Earnings growth moderates. Earnings up 5.1%.

- 2023: Deficit begins to rise, but smaller deficit from 2022 still felt. Earnings growth flat lines. Up 0.4%.

- 2024: Deficit projected to rise again.

That deficit situation is interesting. Will the deficit actually be tackled?

- In 2009, the United States ran the largest federal deficit in the history of the country (in nominal terms): $1.413 trillion.

- In 2022, the deficit was slightly smaller in nominal terms at $1.376 trillion. It was quite a bit smaller adjusted for inflation.

- In 2023, it was back to $1.695 trillion.

- In 2024, it is projected to be around $1.9 to $2.0 trillion.

Fun fact: The smallest deficit since the GFC (Great Financial Crisis) was from 2014 to 2016.

If we actually see the deficit plunge, that could negatively impact earnings. I’m not trying to forecast where earnings will be next year or some other future year. I’m just a bit cautious about the surge in earnings expectations. The companies are supposed to collectively grow revenues by 5.7% and earnings by 14.6% or 15.0%. They can’t grow all that revenue from charging each other, because then it would just be shifting the earnings. That leaves generating higher margins on sales to the government or sales to consumers.

Portfolio Updates

You can find prior installments of the Portfolio Updates on the Portfolio tab of our website.

Older editions of the Portfolio Update are unlocked for everyone. The newest release reserves the foreshadowing section for paid members (for a couple of weeks).

Trade Alerts

We have a page on our REIT Forum website to link all trade alert articles.

Here are The REIT Forum’s trade alerts.

Layout - Modified Order

To keep things simple for our investors, the rest of the portfolio update is divided into several segments. We run the same segments (with new content) each week.

We usually maintain the same order from month to month, but I revised the order to work better with free previews. Eventually, the order will be locked in again.

- Returns on Total Portfolio

- Sector Allocation

- Reminder About Cash

- Housekeeping

- Recently Closed Positions with Returns

- Recently Opened Positions with Returns

- All Open Positions by Sector with Returns

- Outlook

- Foreshadowing Potential Trades (paid section)

This layout maximizes transparency while keeping the foreshadowing of our potential trades within the paid section. It also loads the images together at the front, while putting the text-heavy sections together at the end.

Returns on Total Portfolio

Note: The presentation of the charts was modified slightly to enable running it through Google Sheets instead of Excel to reduce transferring data.

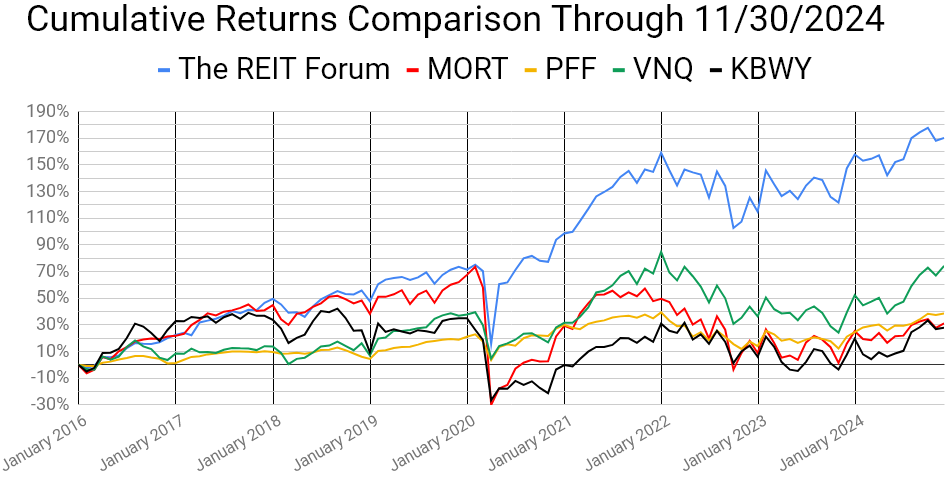

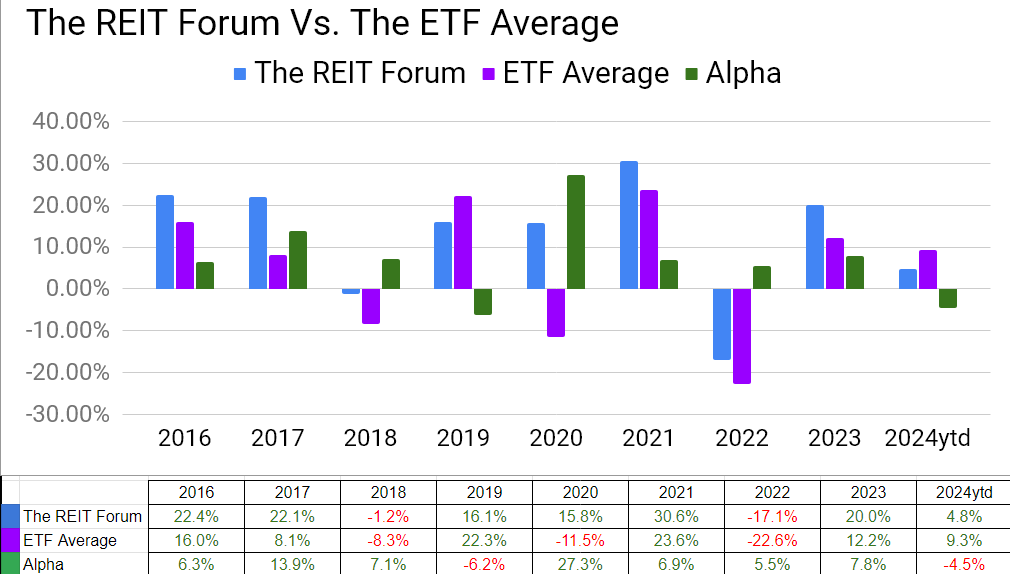

The chart below shows our performance since we began preparing for The REIT Forum at the start of 2016 through the end of the latest month:

There are four major index ETFs we use for evaluating performance. They are:

- (MORT) $MORT - Major mortgage REIT ETF

- (PFF) $PFF - The largest preferred share ETF

- (VNQ) $VNQ - The largest equity REIT ETF

- (KBWY) $KBWY - The high-yield equity REIT ETF most retail investors follow

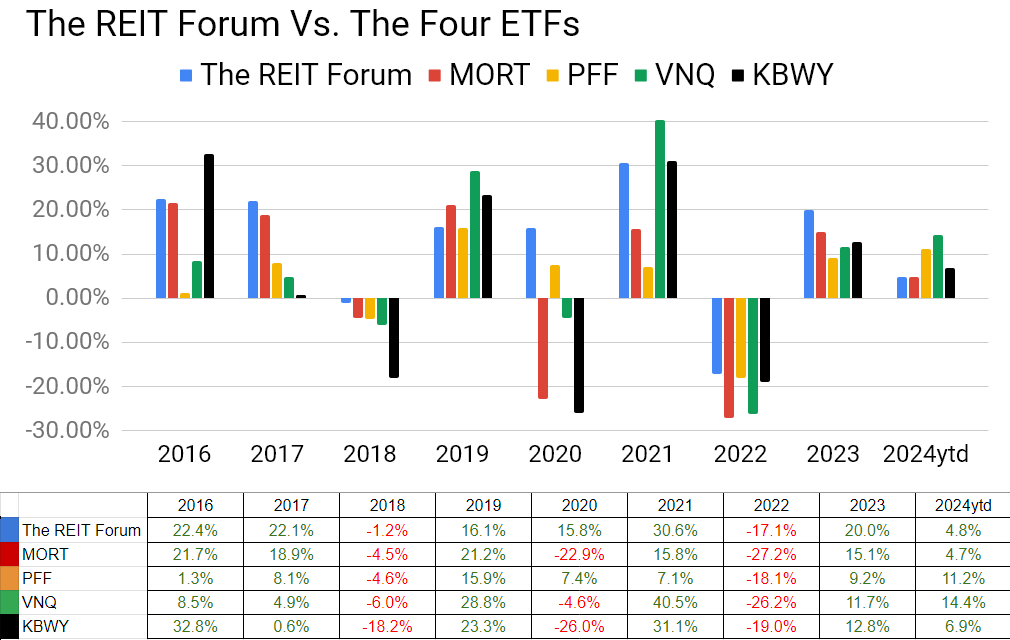

Annual comparison vs. each ETF:

Our performance vs. the average of the ETFs:

We evaluate alpha based on performance against the ETFs because it strips out the general change in our sectors.

We delivered a respectable gain in August, but the indexes took the lead. Trailing this late in the year has been a rare occurrence.

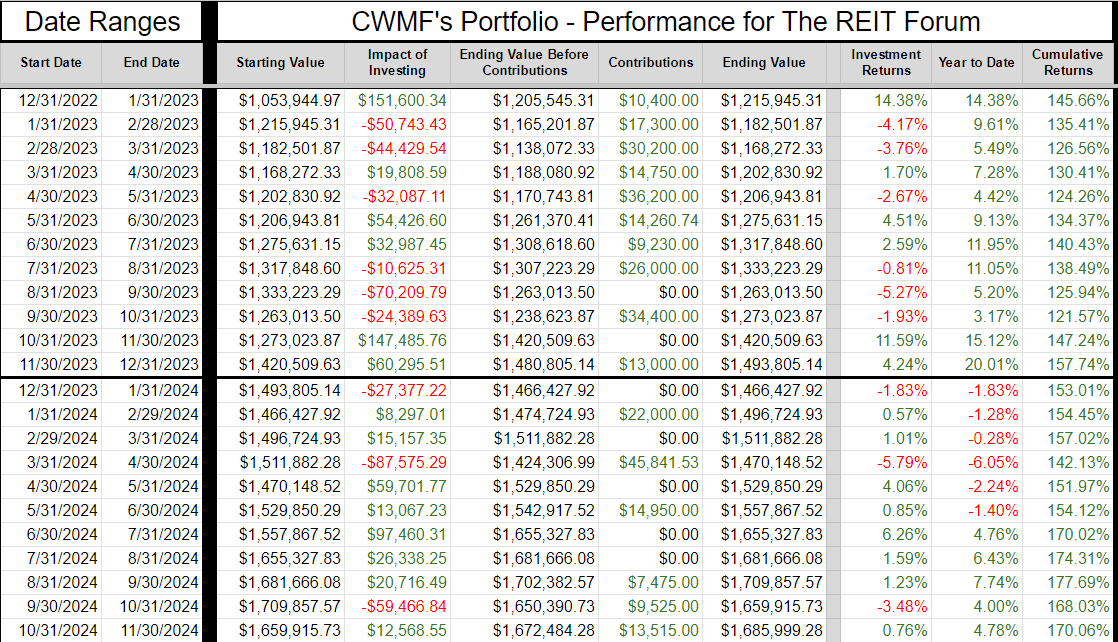

The next chart shows the change in the value of our portfolio from month to month. We strip out the impact from contributions made during the month because, obviously, contributions are not returns.

The prior year is included as well to help investors see how the calculations work.

If anyone is confused by these calculations, let me know. I believe this transparency is crucial, so I’ll include an example showing every calculation if I hear that readers have any difficulty following it.

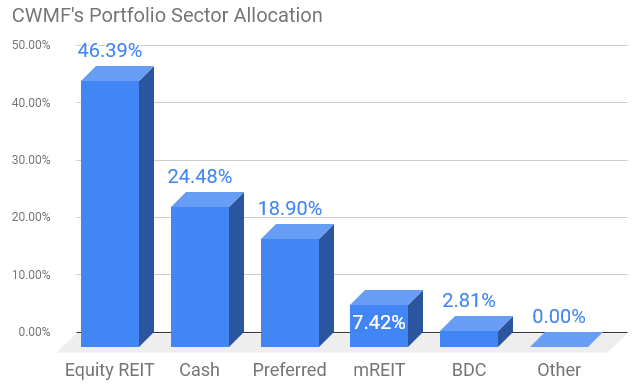

Sector Allocation Chart -

The sector allocation chart helps to explain how we are thinking about risk and seeking returns:

Reminder About Cash (repeated)

I normally keep at least 6 months or more of living expenses in “cash”. If you normally keep around $40k to $50k in “cash”, the difference between getting paid 5% and 0.2% is around $2k per year.

I’m using (SGOV), (SHV), and (BIL) as my cash substitutes. These are short-term Treasury ETFs. Prices are extremely stable. Liquidity is excellent.

I use a Schwab business account that is not part of my portfolio. The only assets it holds are actual cash and cash substitutes (those 3 ETFs).

Nearly all my expenses go through my credit card already (paid off in full each month).

I still have my checking through USAA because of the long history on those credit cards. If I need cash, I can sell Treasury ETFs and transfer the funds to my USAA account.

It takes a few days, but that’s fine.

This is a pretty nice return for cash I was going to have there anyway.

Note: Some people think you don’t need a strong credit score after getting a mortgage. I disagree. The long history on those cards is extremely useful if I want to boost someone’s credit score. If I add someone to my card, their next update will show they have a card with 20 years of perfect history.

You can get scammed this way. You are liable for the bill. They can just charge the card and walk away. This doesn’t concern me because I keep a lower limit (such as $10k) on those cards and I’m only doing it for people I trust. If one of those people betrays me, I’ll count myself lucky that I found out for only $10k. For people who can’t afford to risk that money, this would be too dangerous.

Housekeeping

We used to have a repeated section on strategy, but I wanted to shorten the update.

I’ll be posting an article that covers our strategy in greater depth and just adding a link to that post.

We have a project underway to update our guides and improve the organization.

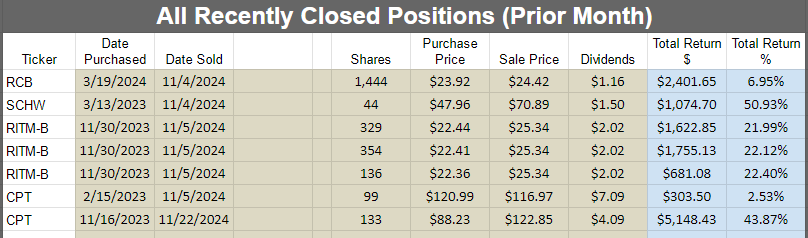

Recently Closed Positions with Returns

These are the positions closed during the prior calendar month. If you want to see positions that were closed before that, you can see the prior portfolio updates or use the Google Sheets.

If we didn’t close any positions for the sector during the month, then the image will be blank.

Note: By loading the Google Sheets, you can still see all of our closed positions. We only include the recently closed positions to reduce the size of the article:

Recently Opened Positions with Returns

All Open Positions by Sector with Returns

We will start with the open positions as of the end of the month. It often takes a few days to prepare this article, but the screenshots below are from the end of the prior month.

The cell with the ticker is grey if the position is in a taxable account. This was a request by a few members and there was no drawback to adding the information. All of the taxable positions are in equity REITs.

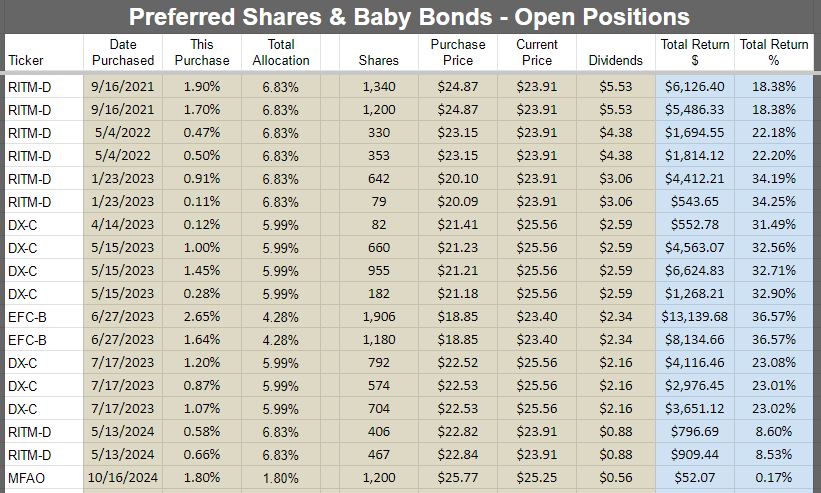

Preferred shares and baby bonds:

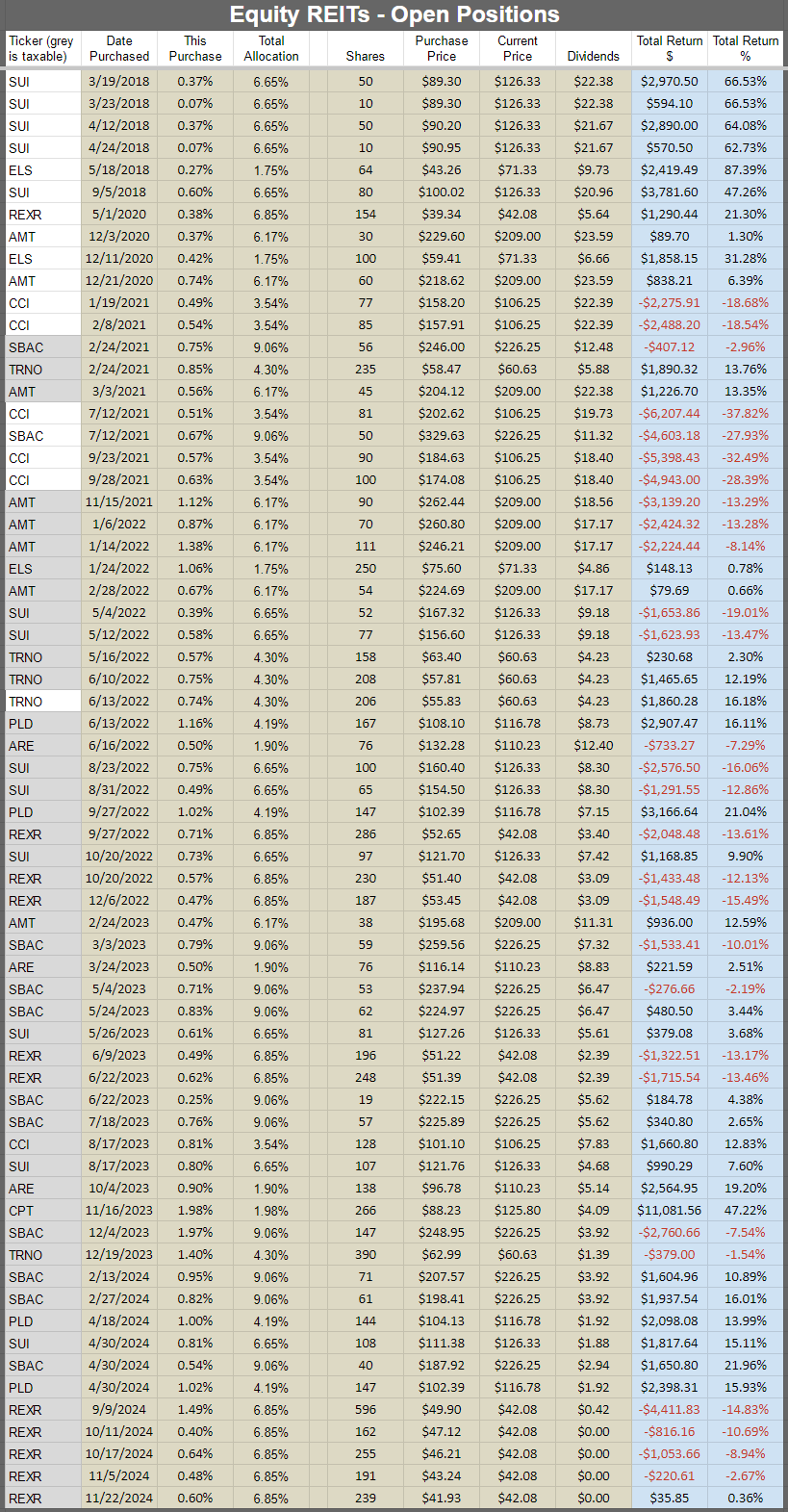

Equity REITs:

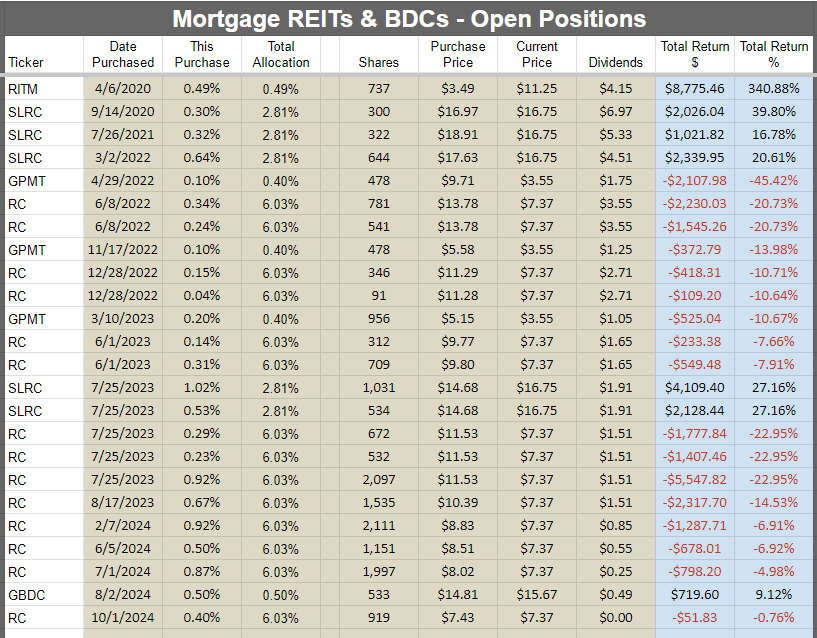

Mortgage REITs and BDCs:

Other:

Subsequent Changes

None so far.

Foreshadowing Potential Trades

This section is usually prepared shortly before publishing. The goal is to quickly cover ideas for trades. We aim to foreshadow our trades here, though the market may move in surprising ways. While the article takes days to prepare and documents prices and performance from the end of the month, the potential trades section is written last to provide the most up-to-date pricing.

Based on the change in relative prices as of 12/03/2024 here are some of the trades on my radar.

Note: Some prices are end of day, some are during trading. It takes a bit to prepare this section for subscribers.

Paid Section Begins

Potential Preferred Share (and Baby Bond) Trades

AGNCO (AGNCO) could be interesting. It closed November with a dip that was quite appealing, but it popped higher immediately. I would consider playing with shares occasionally based on their discount relative to AGNCN (AGNCN). The annualized yield to call isn’t great (around 5.7%), but that’s based on an immediate call. If shares remain outstanding, the floating yield is in the high 9% range. So each day they don’t get called is an improvement. If they do get called, well the 5.7% annualized rate isn’t the worst thing in the world. It’s certainly not enough to ruin my day.

DX-C (DX-C) (DX.PR.C) could be interesting. It should trade in a fairly tight range. If it spikes higher, I could close some or all of my position. If it dips, I could raise the position. For reference, it’s $25.34 as I’m writing. I would expect shares to trend higher a bit faster than dividend accrual because the floating spread would be so attractive. But I also see a significant level of call risk. In this case the annualized yield to call is about 5.8%.

RITM-C (RITM-C) (RITM.PR.C) could be interesting. Great annualized yield to call at 15.9%. However, the floating spread is a bit thin relative to the risk rating. Consequently, it might trade a bit under call value (adjusted for dividend accrual) while floating. Therefore, the realized return for a trade would probably be quite a bit lower than the annualized yield to call.

PMT-A (PMT-A) (PMT.PR.A) and PMT-B (PMT-B) (PMT.PR.B) could be interesting. I would like to get an update published on the court case. They don’t make it particularly easy to find the relevant documents. The defense seems weak, but the prosecution (looking to force the floating rate) may not be pounding on the issue of synthetic LIBOR, which seems to me like it should seal the case.

MFAO (MFAO) bumps around a little bit. I would expect it to have a fairly tight trading range. If shares rally faster than interest accrual, I might close it. But if shares don’t increase with interest accrual, I might add a bit. Shares are currently at $25.22. Interest accrual should cause that price to trend higher by about $.06 per 10 days. On ex-dividend dates, it should drop by about $.56.

Potential Common Share Trades

Realty Income (O) finally lands on the list. It seems every time Realty Income hits an attractive level, there are other shares that are more attractive. That is still the case if we look outside the net lease sector, but Realty Income stands out on the dip valuation relative to most peers. W.P. Carey (WPC) has seen a weaker price also, but WPC has a higher risk rating and weaker management. So at similar valuations, I’ll favor Realty Income. It’s simply been very hard to find an attractive entry point for the shares. Realty Income had a bigger discount to targets in July, but O actually underperformed Agree Realty (ADC) and Four Corners Property Trust (FCPT) over that period. I’ll probably initiate a small position in Realty Income.

It may not sound positive, but Realty Income’s growth over the last few years required them to issue a fair amount of debt at higher rates. Consequently, the average rate on their debt is already 3.92%. They have access to European bond markets, so they can get a lower average cost on debt. What that means is that rolling over debt to market rates becomes a smaller headwind. Two years ago, Realty Income’s average rate on debt was 3.15%. So the REIT has done a pretty good job of growing despite the headwind from higher average rates. At $56.05, Realty Income trades at about 13x forward AFFO projections of $4.30.

- Guidance: $4.17 to $4.21 (midpoint $4.19).

- Consensus 2024 projection: $4.19.

- Consensus 2025 projection: $4.33.

The forward 12 months estimate for $4.30 will include Q4 2024 instead of Q4 2025.

Due to external growth requiring the total size of the REIT to grow significantly, the growth rate in future years may be lower. But management may be able to delay those headwinds for quite a few more years. If interest rates fall, it could be a nice boost to AFFO growth in the future since rates would reset lower instead of higher.

Alexandria Real Estate (ARE): Shares have been quite weak. I’ll have to think about adding here. The sector has been facing elevated supply, much like many other sectors. Annual guidance still looks fine. ARE is a bit different from many of my picks. At $108.89, Alexandria trades at a fairly low AFFO multiple (14.22x forward estimates of $7.66) relative to the rest of the equity REIT sector. Note: AFFO includes adjustments for maintenance capital expenditures, so the AFFO estimates are much lower than management’s guidance for “FFO as Adjusted”.We usually pick REITs that trade at higher AFFO multiples because of their strong growth rates. Consequently, ARE stands out a bit in the current environment. Their debt relative to the market cap of equity is getting a bit high, but the balance sheet is still pretty strong and they have exceptionally long maturities on their debts. Other debt ratios look good. Net debt and preferred equity to adjusted EBITDA was 5.5x with a target for Q4 of 5.1x. What level is okay there? It depends on the type of real estate. But typically we’re fine with anything around 6.0x or lower. They can have a higher multiple if their real estate tends to trade at lower cap rates, because then the net debt to the value of real estate would still be lower.

That might have been a bit confusing. If the real estate trades at a low cap rate, that means the real estate has a high price relative to the net operating income it produces. A higher price for the real estate typically reflects expectations for faster rent growth, or a property where the expiring lease is well below market rates. The highest cap rates go to properties where rents are likely to fall (such as low-quality malls). Those properties have a lower price relative to net operating income because the future net operating income will likely be much lower.

If a REIT owns trashy real estate (like low-quality malls), then 6.0x could be very high.

Rexford (REXR) stays on the list, but I’ve already increased the position quite a few times. I’ll have an update coming on industrial REITs that will result in moderately lower targets to reflect the increased tariff risk. There’s no certainty presently about what level of tariffs will exist in the future, which countries they will be applied to, or how they may be circumvented.

Equity Lifestyle (ELS) or Sun Communities (SUI) could be interesting. They’ve been much weaker than the apartment REITs lately.

Camden Property Trust (CPT): Depending on valuation (currently $123.51), I could continue to reduce my position in Camden Property Trust. I still like the exposure to their apartment portfolio, and I still trust management. However, valuations remain an important consideration. CPT has been pretty strong compared to most REITs. Less new supply in apartments should be great, but it’s strange to see the different types of equity REITs diverge so far from each other.

Potential Trade Summary

To summarize:

- Interested in AGNCO if we get a dip. Would probably be a short-term trade looking for shares to achieve a negative yield-to-call in the future.

- DX-C and MFAO could go either way depending on valuation. Expecting fairly tight ranges.

- RITM-C might be interesting because of the high annualized yield to call, but I think shares should trade at lower valuations than RITM-B and RITM-A.

- PMT-A and PMT-B could be interesting plays on the potential outcomes for the trial. I’d like to have more info on everything happening inside the court room.

- O finally gets on the list. It’s not as cheap as some of the other equity REITs, but it is within our target range and trades at a lower price-to-buy than peers. I would be inclined to keep the position small (unless shares got crushed).

- ARE is also back on the list after some weakness brought the multiple down again.

- REXR is interesting and I really like the valuation. However, I’ve also been growing this position quite a bit already.

- ELS and SUI could be interesting. Weaker relative performance to apartment REITs. How long will that continue? MH parks can benefit from reduced apartment supply and lower gas prices would be quite favorable for the RV parks.

- CPT is still a candidate for taking profits (selling some shares). Nothing wrong with CPT, but shares are trading slightly above 21x forward AFFO.

Conclusion

Thanks for reading. I hope you find the ideas in this article helpful as you navigate the markets.

I apologize in advance for any typos. With such a large document, having at least one or two is common. If you caught any, let me know in the comments. If you’re reading this more than a day after publication, check the comments section for any corrections.

Disclosure: Long positions shown in my portfolio.

Member discussion