PennyMac Preferred Shares and the Obvious Lawsuit

PennyMac Mortgage Trust (PMT) gets two articles for PMT-A (PMT.PR.A) and PMT-B (PMT.PR.B).

One was a boring piece. The rough draft for that was pretty quick.

However, there were a few more things I wanted to say.

Next thing you know, I’ve got this huge article that swings between dull and exceptional.

Why are there two separate articles?

By the time I was done writing the parts I wanted to write, there was no way it would pass editorial at Seeking Alpha.

Not an issue with the quality research. Don’t be silly.

The parts I wanted to write are simply too good. They are too engaging. They speak frankly and use some outstanding images.

Consequently, I split the article into parts:

- One for my personal fans.

- One for Seeking Alpha Premium.

This is the one for my personal fans.

This is the part I actually wanted to write.

It contains sections that Seeking Alpha definitely would not have published.

Ghost

Note: If you're subscribed to our Substack page, you're already subscribed here. I imported our membership data this morning. Ghost will be our new primary channel.

If you are not already signed up for Substack, just subscribe to our ghost page here to get started. There's a free option, so if you like our work, there is no reason not to do it.

There is no need to change your bookmarks. Our domain will host the ghost page soon. All paid memberships are also being copied over. I've designed this process to be smooth for our members.

Switching to Ghost is allowing us to significantly lower prices.

Back to the article!

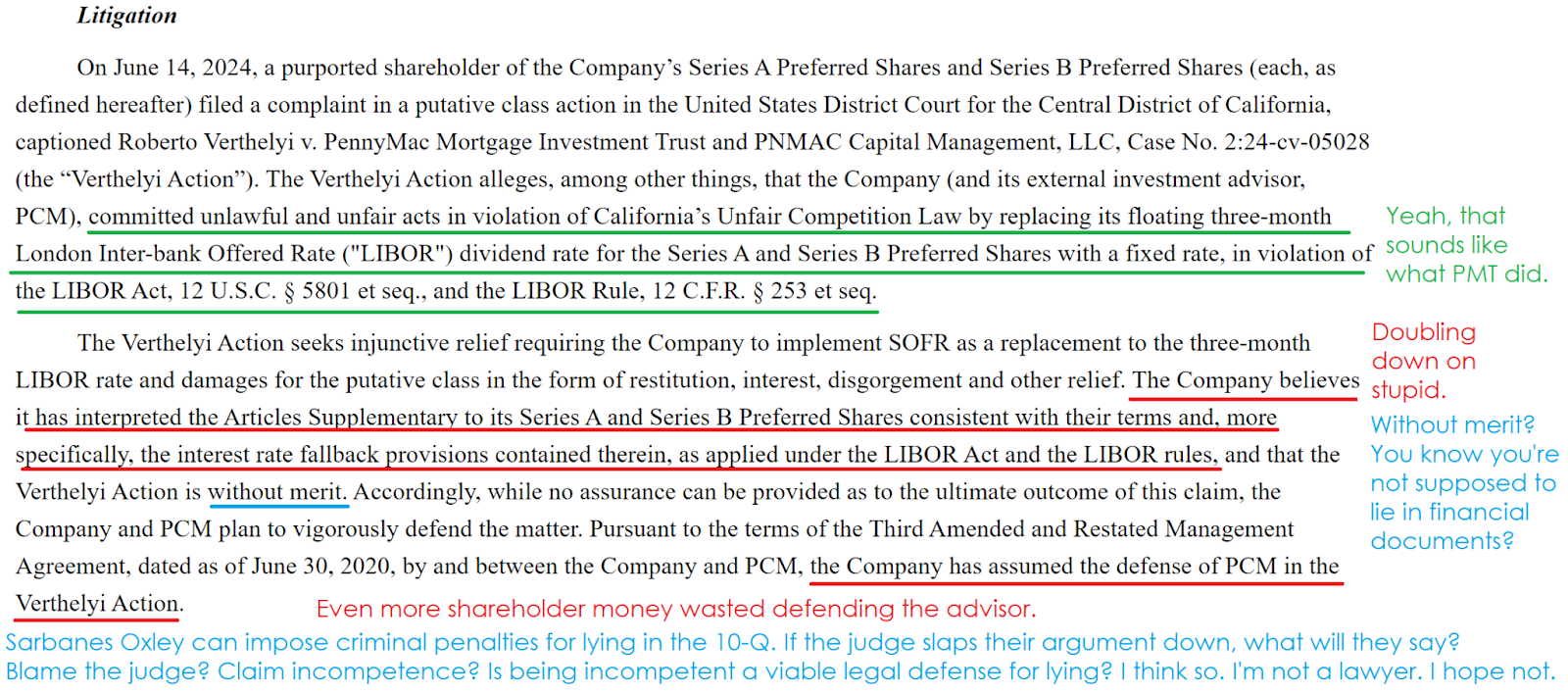

PennyMac’s Disclosure

PennyMac disclosed the lawsuit in their 10-Q:

I believe their decision to fight these charges is absurd.

The decision to use boilerplate language about a lawsuit being without merit should be investigated. Don’t worry though. Most likely they won’t have any personal consequences. Shareholders will eat the costs, but management will be fine.

If you’ve got the right prompts, you can get some perfect images. That’s just baking powder on the mirror.

The Prospectus for PennyMac Preferred Stock

In my prior articles, where I absolutely demolished PennyMac’s defense, I didn’t have the following image.

The beauty of this case is that PMT can lose it in so many ways.

Whatever argument they want to try, it gets demolished.

Since PMT decided to reference the fallback provisions in their 10-Q, I’ll tackle that specifically.

I’ve added some highlighting to demonstrate how the clauses work:

PennyMac and the Fallback Provision

PMT is trying to activate a clause that does not activate.

In my prior work, I demonstrated why that clause won’t save them either.

PMT argues that the “preceding dividend period” is a “practicable” benchmark. Therefore, they “believe” that they have a practicable benchmark. If they don’t have a practicable benchmark, their entire argument falls apart and they are left just paying legal fees.

Now, some readers are going to wonder if synthetic LIBOR is really a thing.

Here is the ICE Benchmark Administration stating that it is compelled by the UK Financial Conduct Authority to publish 1, 3, and 6-month USD LIBOR.

ICE refers to it as “using an unrepresentative synthetic methodology”.

Non-Representative LIBOR

If ICE says that 3-month USD LIBOR is not representative, does that give PMT a way to escape?

No.

According to the rule published by the Federal Reserve, it does not.

Here is the relevant commentary:

If PMT is able to claim that they are not covered by the statute, then their contract ends at the first step of the waterfall.

The rate existed. They just didn’t like it. Not liking the interest rate is not legal grounds to unilaterally change a contract. I’m not a lawyer, but I sure think I got that right. Any of the lawyers can reach out and let me know if a single party can revise their contract because they don’t like the interest rate.

I did a search for “representative”. The term only shows up twice in the prospectus. In both cases, it is within the section about rate quotations and it pertains to the dollar amount of a transaction, not whether the rate was representative.

Conclusion

If PMT were to win this case, it would rewrite the very concept of words and laws.

Sometimes a great lawyer wins a case even when their case is objectively stupid.

It isn’t easy though. They would have to overcome all these hurdles like facts, laws, and the meaning of words.

Disclosure: Long PMT-B, PMT-C.

PMT-C ($20.11) is in the neutral range. As a fixed-rate share, it has upside if rates fall further without a major recession. It has downside if rates rally.

Rating PMT-B is more difficult. PMT-B ($24.49) is trading within pennies of our “buy under” target ($24.53).

It’s not low enough that I would want to publish a fresh bullish rating (it was two weeks ago), but I don’t really want to swap to the neutral stance either since it could still rally.

The timeline for a decision on the case is unclear to me, but it seems like a remarkably easy case. Much easier than deciding which way to rate a share that is about 0.2% from a price target.

I haven’t decided whether I’ll tag it as bullish or neutral. I’ll probably submit the article during the evening (maybe today, maybe tomorrow) and use the closing price to determine which rating to put on it.

I don’t think the rating matters nearly as much as the argument though.

Otherwise, check out a few more free articles:

Realty Income Q2 2024: Acquisitions Fuel Growth

Demolishing an Awful Article on AGNC

Edit: Comments should be available now. Had to enable the feature.

Member discussion