Net Lease REITs: Q2 2024 Target Updates

Brief Version

This article took a bit longer to prepare. I was trying to find an answer for precisely where I went wrong.

I did some extensive research on the net lease REITs while setting targets before. The thesis looked great. It was built on solid accounting.

Despite the research, National Retail Properties (NNN) significantly outperformed my expectations. I initially brushed this off as the market overreacting to inflated figures.

Upon digging in, I came to three conclusions:

- National Retail Properties had a couple of really good years. Not as good as the market seems to think, but still really good.

- I didn’t adjust for differences in relative performances that could be expected in the underlying real estate portfolio based on property type. Seems like a silly thing to miss, but the timing was brutal. This was right after Realty Income (O) made upgrading their portfolio look easy. In hindsight, what Realty Income did was the equivalent of hitting a full-court shot with half a second on the clock.

- Our negative adjustments to W. P. Carey (WPC) based on management’s stupid plan (spin properties & cut the dividend) were accurate. However, I was a bit too gentle. I didn’t adjust for some weakness in the real estate. This was a bit surprising because the listed property types should be outperforming. Industrial and warehouse space should be good! Their retail shouldn’t be falling so far behind peers.

Target updates are included below:

Note 1: We adjusted targets for Realty Income 2 to 3 weeks ago. They were +3.5%. No further adjustment is needed at this time. Therefore, we are reiterating the prior targets from August 8th, 2024.

Note 2: If you just wanted the updates and reasoning, you’re up to date. I’ll go a bit deeper for investors who want it.

Full Article Begins

To dive into this, we should step back in time.

The AFFO and Revenue Timeline

I wanted to go from start to finish, but there was a problem. That layout spreads things out across several years. So, I’m going to start with the spoiler:

- NNN’s 2020 results were missing revenue (and AFFO) they could have recognized.

- NNN’s 2021 and 2022 results would have bonus revenue (and AFFO) from their actions in 2020.

- NNN’s 2023 to 2025 results would see progressively smaller benefits.

That was roughly how things have been playing out. Yet something else was off.

NNN’s real underlying performance was better than I was giving them credit for.

Not dramatically better, but still materially better. Well done to National Retail Properties.

They hammered that point home by raising guidance again in the Q2 2024 earnings release. AFFO per share guidance is only up 0.6%, but that’s still a solid boost for a Q2 earnings release.

The headwind still exists for future years, but the total headwind remaining is less than 1% of AFFO per share. That should occur across multiple years, so it is basically a non-issue today.

Now that you know what happened with the numbers, we can step into the analysis process.

When National Retail Properties Was Punished

In late 2020, I argued that NNN was being unfairly punished because of conservative accounting. NNN was being very careful not to recognize revenue unless they were confident the tenant would fulfill the terms of the lease. They also modified several leases to give tenants a bit more time to catch up on rent. I argued during 2020 that NNN was being prudent in their relationships with tenants, though the careful revenue recognition would create issues down the road. NNN wasn’t giving up cash. They were giving time and being careful not to book revenues too early. It was good management, though some investors criticized management for being so prudent with their customers.

This was one call I got precisely right.

When Realty Income Revealed Their Plan

That thesis was playing out precisely as I expected in late 2021. Meanwhile, Realty Income (O) had a great deal. It looked okay at the time, but not great.

In mid-to-late 2021, Realty Income swung two deals together. The combination here was the masterpiece. Neither deal alone would’ve been so great.

These are the two transactions:

- Realty Income acquired VEREIT (VER).

- Realty Income announced they would spin off their crappy (office, okay, crappy is a euphemism for office) properties.

If we exclude the office properties owned by Realty Income, their average portfolio quality was better than the stuff owned by VEREIT.

The deal was going to be accretive to AFFO, but that didn’t seem too impressive.

However, Realty Income lined this up perfectly.

The Realty Income Combination

Realty Income drilled the timing:

- Inflation escalators were giving REITs moderately better revenue growth for 2022.

- The acquisition of VEREIT was driving AFFO per share growth.

That combination meant Realty Income could announce strong AFFO per share growth (and easily cover the dividend) even though they were ejecting some office trash.

To be clear, office properties were not a large portion of Realty Income’s portfolio. It was only 3.0% before the merger with VEREIT. However, adjusting for leverage, spinning those properties off should’ve hit AFFO per share for more than 3%. That would’ve made growth look bad for a year. By doing these transactions together, Realty Income was able to provide a much more compelling story to investors.

In this case, I was right about the value of the transaction with VEREIT but didn’t realize how difficult it would be for any other REIT to achieve something similar.

When National Retail Properties Roared Back

National Retail Properties performed well over the last few years.

I attributed a bit too much of their recovery to the impact of the deferred revenue and AFFO.

Consequently, I didn’t adjust them as early as I should have.

I expected the market to be disappointed about slower growth. The market often overreacts to some short-term headwind, so it seemed likely here.

After all, we saw the market overreacting in 2020. Yeah, there was this whole financial crisis thing with the pandemic. But NNN was overly punished.

It seemed reasonable that history would repeat itself, but it didn’t.

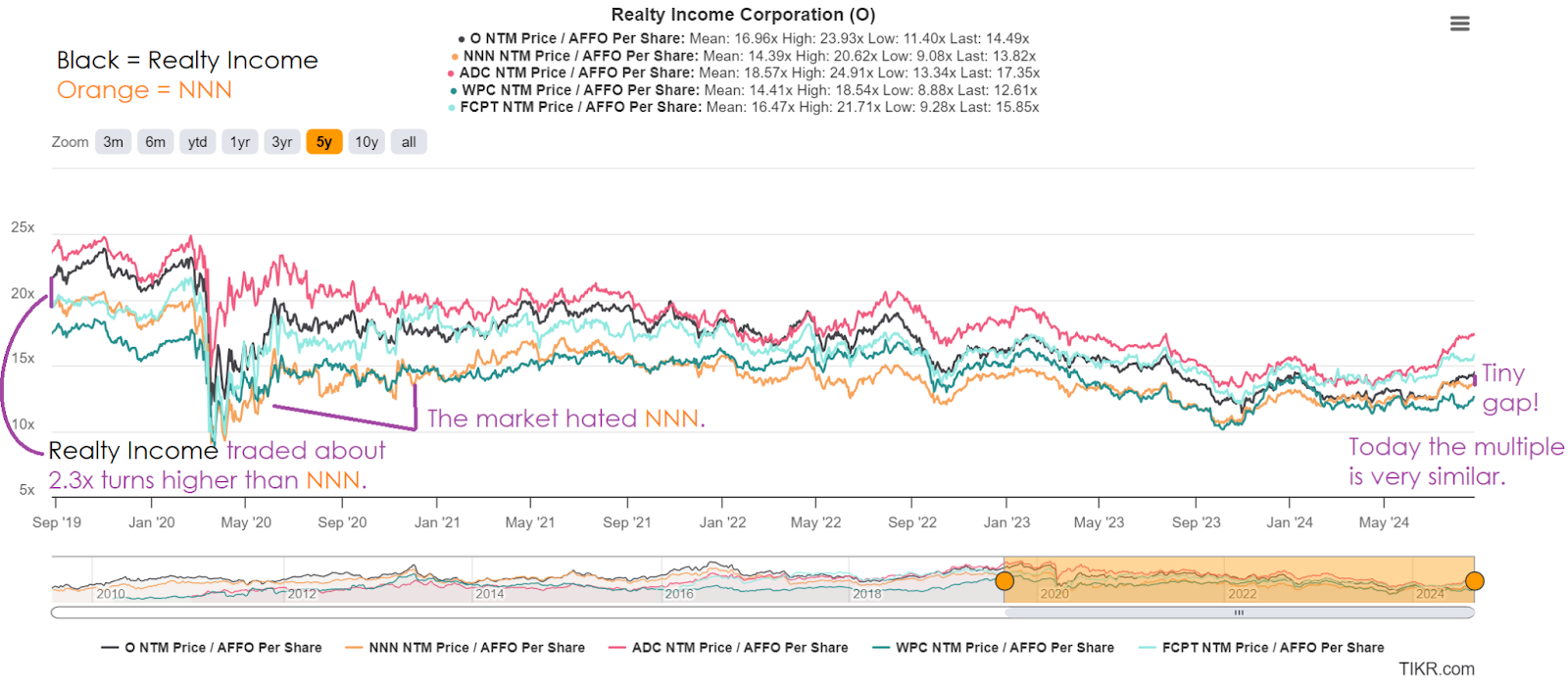

The Swing in Multiples

Over the last 5 years, we saw a significant swing in the AFFO multiples:

Realty Income often traded at a higher multiple than National Retail Properties. That’s become ingrained as normal.

It reached an absurd gap at times given the REITs typically have similar amounts of leverage. The portfolio quality is usually expected to be similar as well. But Realty Income has the “Monthly Dividend Company” tag and is actively acquiring other companies (great for growth), so they often get a bit of a higher multiple.

In my opinion, the multiples today are too close.

I’m expecting the typical difference in AFFO multiples between O and NNN to be about 2x AFFO.

Where W. P. Carey Disappointed

At this point, we all know about management’s blunder. They destroyed dividend aristocrat status. There is no justification for it, and I won’t try to give them one.

We can evaluate their reasons, but ultimately it was a stupid decision.

That’s fine. We already knew that. WPC’s AFFO per share is struggling as a result of spinning off those office properties. Is that all it is though?

We know WPC reported weak “same-store achieved rent growth”. That looks like a more convoluted term for “same-store revenue” to me.

That shouldn’t be confused with “contractual” rent growth. Under the contracts, WPC is due about 3% annual rent growth currently. Therefore, year-over-year the growth rate should be about 3%. However, situations with these tenants (deadbeat tenants) negatively impacted actual rent collections.

One of the differences between the headwind NNN faced with tenants in 2020 and the challenge WPC faces today is the lack of a pandemic. Unlike 2020, tenants are not forcibly closed for business. These tenants are simply failing on their own. Because the tenants are at fault, WPC should be telling them to pound sand.

Valuation

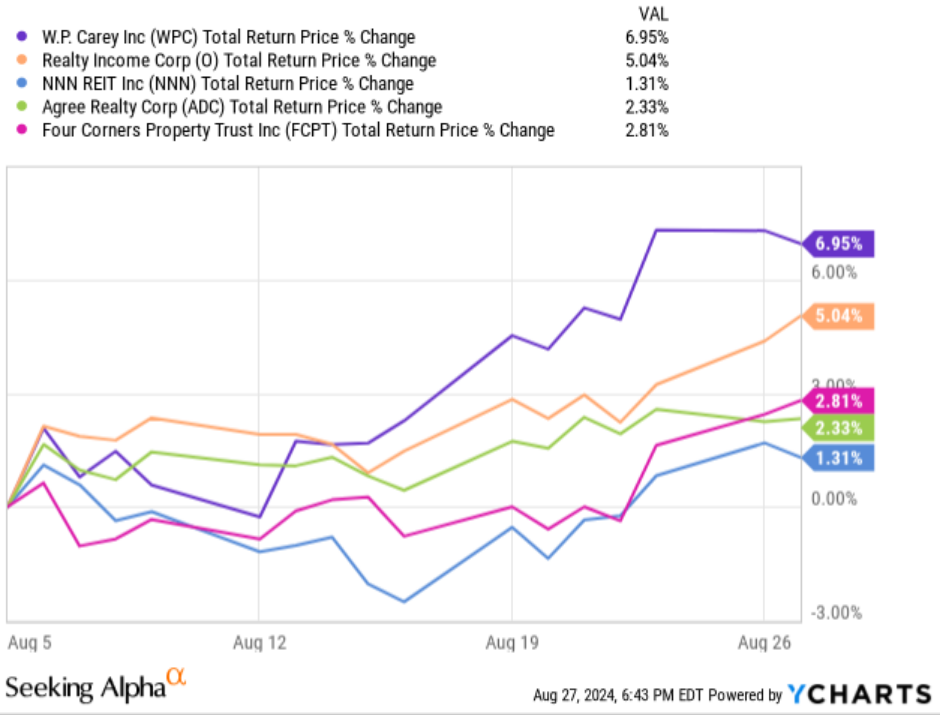

When I reviewed WPC’s Q2 2024 earnings a few weeks ago, I wrote:

“I find WPC the most attractively valued of the net lease REITs.”

Since that article, WPC has indeed delivered the best share price performance among the net lease REITs we cover:

Prices as of market close on August 27th, 2024.

Following the adjustments, none of the net lease REITs lands within our target range for buying. However, the closest two are still O and WPC. WPC has a slight edge.

I may provide an article providing more of a comparison between the lease REITs if there’s interest in the topic.

Such an article could be a useful point of reference for investors in the sector for quite a while. Consequently, it would focus less on valuation and more on the details of the REIT. Valuation is important when it comes to deciding whether to buy, but the underlying real estate (and management) can be evaluated separately.

Conclusion

No adjustment to Realty Income since they had one recently.

The biggest adjustment in the sector by a substantial margin goes to National Retail Properties.

They simply performed better than I expected over the last few years. The 2020 AFFO figures were artificially bad and the subsequent AFFO figures were artificially good. However, despite the artificial increase in AFFO, there was also a substantial legitimate increase. National Retail Properties simply outperformed my expectations for the REIT.

Presently, shares of NNN trade at a slightly AFFO multiple relative to Realty Income (13.80x vs 14.53x using forward consensus AFFO).

I still think the typical gap will be a bit bigger, so I would still favor Realty Income relative to National Retail Properties on valuation. However, I previously established a gap that was too large.

Agree Realty (ADC) gets a small bump to targets. Similar to Realty Income.

Four Corners Property Trust (FCPT) also gets a small bump to targets.

The only reduction goes to W. P. Carey. That adjustment is driven by a reassessment of their performance and expected growth. Things should be improving with the portfolio purged of office assets and the refinancing of debt complete. The higher rate on debt will still weigh on the second half and create a headwind for the first half of 2024. However, WPC has a substantial amount of cash on hand (more than $1 billion) which should be immediately accretive when deployed. The deployment of that cash should create a tailwind. Likewise, the 2025 growth rate should have a tiny boost from Hellweg paying rent for the full year instead of getting the first quarter for free. That had a $.033 impact on revenue and AFFO per share in Q1 2024, so simply collecting rent next year provides a tailwind of nearly $.033 per share (about 0.7%).

Disclosure: No position in any of the REITs mentioned in this article.

Member discussion