First Preferred Share Call of the Season: IVR-B

This morning a call was announced by Invesco Mortgage Capital (IVR) for their fixed-to-floating share: IVR-B (IVR.PR.B). This is the first among the preferred shares we're covering, but more calls may follow in the next few months and certainly in 2025.

Shares of IVR-B will be called effective 12/27/2024, which is the first day they could be called. IVR-B had a spread of 5.18% over 3-month LIBOR (which is defined as 3-month SOFR + 0.26161%). That’s only slightly higher than some of the shares from Annaly Capital Management (NLY) and AGNC Investment Corp. (AGNC).

I'm a bit surprised about IVR-B being the first call, given that shares would have had only a slightly higher spread than peers with better coverage metrics.

I’m projecting the total remaining cash payouts to be about $25.00 + $.484375 for dividends. Yesterday shares closed at $24.88. Therefore, I’m projecting buyers at that price (which probably won’t be available this morning) would have a yield to call of about 18% and a worst-cash-to-call of $.604.

Note: The REIT Forum Google Sheets had the worst-cash-to-call estimated at $.606, so I’m very happy with that estimate.

IVR-B was in our “overpriced” category because the IVR preferred shares have dramatically less coverage than the AGNC or NLY preferred shares and only a tiny bit higher yield.

Note: All calculations in this piece are based on my projection for future cash flows. If I’m wrong about them (hasn’t happened yet to my knowledge except for the MFA call scenario, discussed later), it would change the relevant yields.

Investors would probably be interested in bidding below about $25.10. That would give them an annualized yield to call of about 11.25%.

By $25.20, I would favor taking the cash. That’s an 8.2% annualized yield to call.

By $25.30, I believe investors should absolutely take the money and run. That would put the annualized yield to call around 5.22%.

Note: Investors sitting on a short-term capital gain that would become a long-term capital gain by holding until 12/27/2024 would almost certainly want to sit on their hands and wait for the call. This is not tax advice.

When a call like this is announced, the company is not actually legally forced to execute the call as announced. It is still possible for them to back out. Consequently, investors should demand yields higher than bond yields. This was seen during the pandemic. MFA Financial (MFA) had announced a call shortly prior to the pandemic, but backed out of it to protect their common shareholders. At that point, MFA simply couldn’t afford to give up that cash. That’s part of why investors should still see some risk here.

Note: It took slightly longer to prep this article than we had before the market opened.

Update

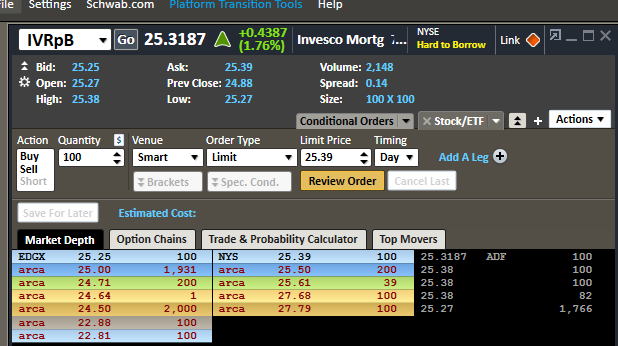

Here’s the first couple minutes of trading on IVR-B:

Source: StreetSmart Edge

At the $25.25 bid, the yield to call is 6.7% (assuming I’m right on the cash flows). That's a pretty good bid.

If investors can get higher prices, as we’ve seen on all executions so far, the yield actually goes lower. Therefore, I believe investors who own these share should be playing with limit-sell orders to take their gains and walk away. Especially if they are able to get someone to pay $25.30 or above. The 5.22% yield to call is only slightly better than what the investor gets for sitting in Treasury bills.

Given the way people are with round numbers, I would be more inclined to fish for buyers at $25.29 than $25.30.

Congratulations to any investors still holding these shares. They've achieved the rare case of a call being announced while shares are still trading at a slight discount to call value. Why isn't IVR just repurchasing all these shares? Low liquidity.

One last note. This may have a negative impact on prices for other shares with a negative yield-to-call. Since many of those shares had superior spreads for lower risk, this call may make investors wary of the risk that their shares could also be called.

Disclosure: We have a position in MFAO, which is a baby bond from MFA Financial. Not really relevant to this article, but I added the disclosure because we referenced MFA Financial briefly.

Member discussion