Digital Realty Income Prints Shares to Buy Treasuries

Digital Realty (DLR) is not one of my favorite REITs, though the market sure does love it. After 7 years of near zero growth in per share metrics, management is shouting “this time is different”. Management is hyped about their success.

Note: Too long? The conclusion section summarizes the article very briefly.

2024 was the kind of year every REIT executive dreams of:

- Reporting Core FFO per share 1.67% higher than in 2018. Compound annual growth rate under 0.3%.

- Reporting AFFO per share 0.83% higher than in 2018. Compound annual growth rate under 0.2%.

That’s the kind of growth that causes CEO Andy Power to declare 2024 a “breakout year”. His words, not mine.

- Digital Realty reported all time record Core FFO per share at $6.71 (that’s $.01 above $6.70 in 2022).

- Digital Realty reported all time (non) record AFFO per share of $6.11 (that’s negative $.14 “above” $6.25 in 2021)

To be fair, DLR might’ve set a new record for AFFO per share (by pennies) if it wasn’t for a surge in their maintenance capex expenses.

That surge in maintenance was beyond the values predicted by management around the middle of October 2024. How could they predict how much maintenance capex they would have in the year with about 2 months left to go? I’m not blaming them for “pulling the capex forward” from 2025. I’m suggesting that my definition of “maintenance” and their definition may be different. As analysts noticed the remarkably low maintenance capex, I wonder if DLR feels obligated to mark more of their capital expenditures as maintenance.

Shares, The Only Thing Outstanding

The outlook from Digital Realty is calling for growth in almost every metric. Before we get into that, I just need to mention shares outstanding.

Since DLR reports different numbers for the weighted-average shares outstanding, we’re going to use the number DLR used when calculating AFFO.

- Q4 2023: 312.36 million

- Full Year 2024: 329.90 million

- Q4 2024: 339.98 million

- Additional shares issued during Q4 2024: 5 million

Since those shares were issued during the quarter, the weighted average will reflect a portion of those shares.

Issuing Shares

If DLR barely issues shares in 2025 (unlikely), they would probably see the weighted average shares increase by roughly 4% to 4.5% (very rough) relative to 2024 due to shares issued late in the year and some stock-based compensation.

Issuing shares is very positive for Digital Realty Trust. Without issuing shares, the performance would be much worse.

Normally people think of issuing shares as dilutive, but in this case issuing shares is accretive even if DLR doesn’t do anything besides buy Treasury Bills. Consequently, the REIT is now sitting on a staggering $3.87 billion of “cash”. Of course, the definition for “cash” has long included Treasury Bills since they are certain to become cash very shortly.

This is going to become quite important as we get into guidance.

Guidance

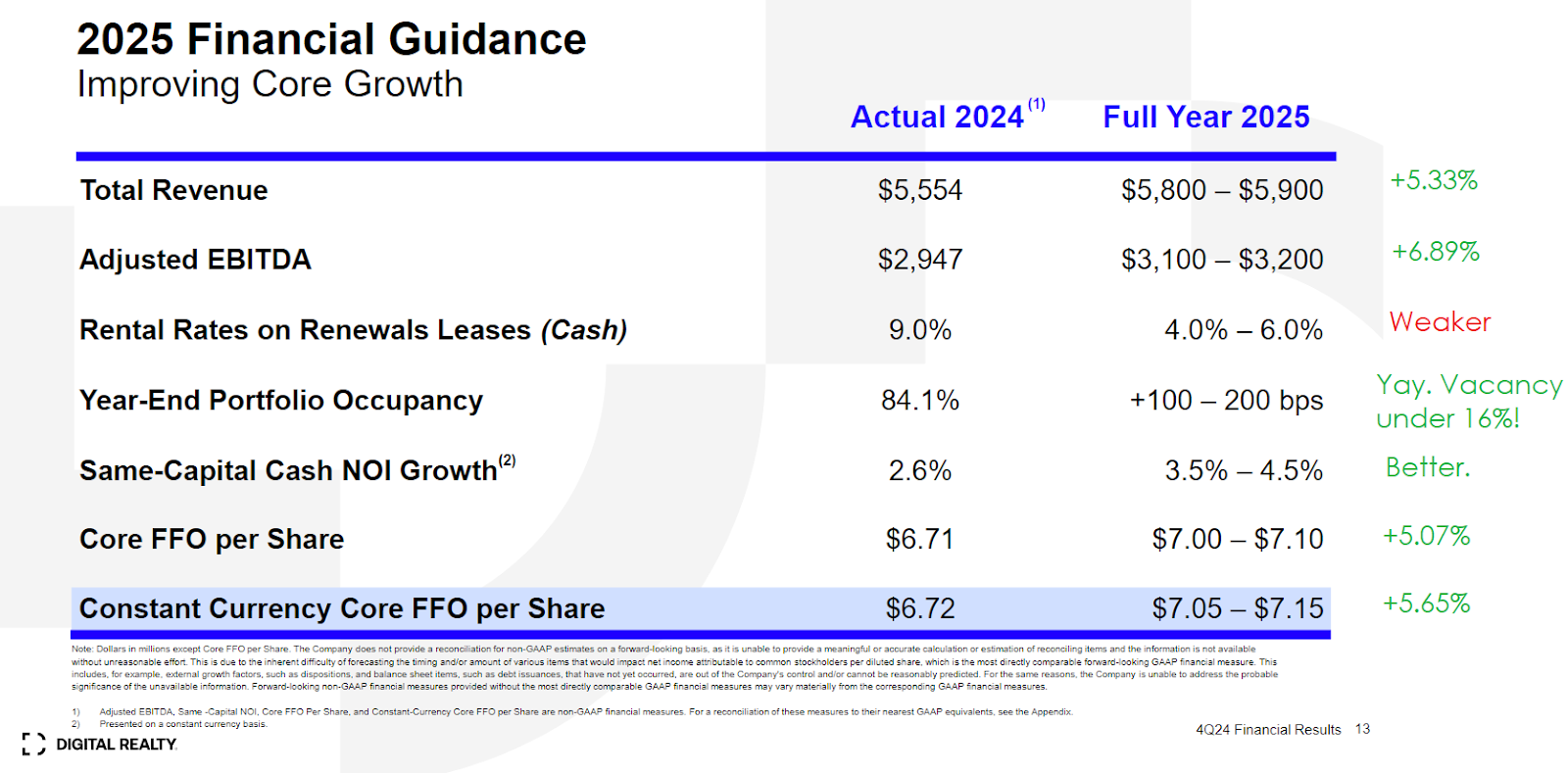

The slide below comes from DLR with my notes added on the right.

We’re projecting shares outstanding would already grow about 4.5% even if DLR wasn’t actively issuing shares. Not issuing shares would be the dumbest possible course of action given their absurdly high share price. But it is important for math.

If revenue goes up 5.33% and shares outstanding go up 4.5%, revenue per share doesn’t increase much (under 1%).

DLR is predicting better adjusted EBITDA margins, as evidenced by adjusted EBITDA growing at a faster rate than revenue. That’s great, if it works out.

If DLR can increase occupancy, then it would make sense for their margins to improve also. Especially if same capital cash NOI grows at 3.5% to 4.5%.

But that brings us to another question.

If revenue per share grows at less than 1% and adjusted EBITDA per share grows at about 2.4%, why is core FFO per share going to grow faster?

Before you come up with some fancy business answer, let me just kill the fun.

The “I” in EBITDA is interest. Core FFO per share factors in interest expense, but it also factors in interest income. That’s where things get fun.

Pump Out Those Horribly Overvalued Shares

DLR was rapidly issuing equity even when they had no obvious use for the capital.

Cash on hand (including Treasury Bills) increased from $1.625 billion at the start of the year to $3.87 billion at the end of the year.

Now why would a REIT want to do that?

Well, the 3-month Treasury Bill has a yield of 4.324%.

When DLR pumps out equity at $185.63 per share (as they did in Q4 2024), they are issuing with the following yields:

- 2.63% Dividend yield.

- 3.29% Trailing AFFO yield (using 2024).

- 3.61% Trailing Core FFO yield (using 2024).

- 3.80% Forward Core FFO yield (using 2025).

What do those numbers have in common? They are all lower than the 4.324% yield on Treasury Bills.

As long as the shares were issued for at least $164.20, investing in Treasuries would be accretive to all of those numbers.

Investors in DLR are willing to settle for extremely low yields on the premise that this time will truly be different.

AFFO and NAV per share are growing as a result of being able to issue shares at very high prices. That’s always beneficial for a REIT, but it also means the growth is dependent on the share price.

Ripping Off My Idea

I previously suggested that the best thing DLR could do was pump out equity and put that cash into Treasuries until they are ready for development projects.

Due to the absurdly high valuation, each time DLR issues shares they are able to:

- Increase NAV per share.

- Increase Core FFO per share (by holding Treasury Bills).

- Increase AFFO per share (by holding Treasury Bills).

That isn’t because the business is doing so great. It’s simply because the share price is that high. This method for building these per share values will only work if the price remains high.

Of course, DLR will probably try to deploy much of that cash into new developments eventually. The yields on development are just too high. We’ll cover that in more detail later.

Note: Many REITs would prefer paying down debts to buying Treasuries. However, DLR’s weighted-average rate on outstanding debts is remarkably low at about 2.72%. Part of the low rate is because Digital Realty issues notes in other currencies where interest rates are lower.

This is Not Normal

No. It is not remotely normal to see REITs trading at an AFFO yield, much less a Core FFO yield, below Treasury rates.

We’ve seen some equity REITs achieve higher multiples than DLR has today (or had recently). However, that mainly happened when those REITS were:

- Growing Core FFO per share at over 10% annually.

- Growing AFFO per share at over 10% annually.

- Treasury rates were much lower, indicating investors had fewer options and the cost of waiting to realize growth was lower.

- The real estate portfolio was on average leased far below market rates, creating embedded growth for future Core FFO and AFFO per share.

Having leases that are below market rates is pretty important because it means there is a substantial amount of growth built into the portfolio. In a scenario where market rents were unchanged, the REIT would continue to report strong growth for several years because the existing leases (which feed into Core FFO and AFFO) would be rolled over to much higher rates.

None of those things are the case for DLR today.

Earnings Call Highlights: Cash Leasing Spreads.

The most relevant one here relates to the cash leasing spreads.

Last year management guided for 4% to 6% cash renewal spreads, but they ended at 9%. That sounds great, but it was driven by a big package deal that pulled forward some leasing on properties that were leased at lower rates. That’s an unusual event and unlikely to recur. Without that one large deal, the cash leasing spreads would’ve only been 5.2% for the full year.

This year guidance calls for 4% to 6% again and management indicated that the lower leasing spreads are because they are still rolling over leases that have higher rates. Management is forecasting that leasing spreads will improve in future years where the average expiring leases are cheaper.

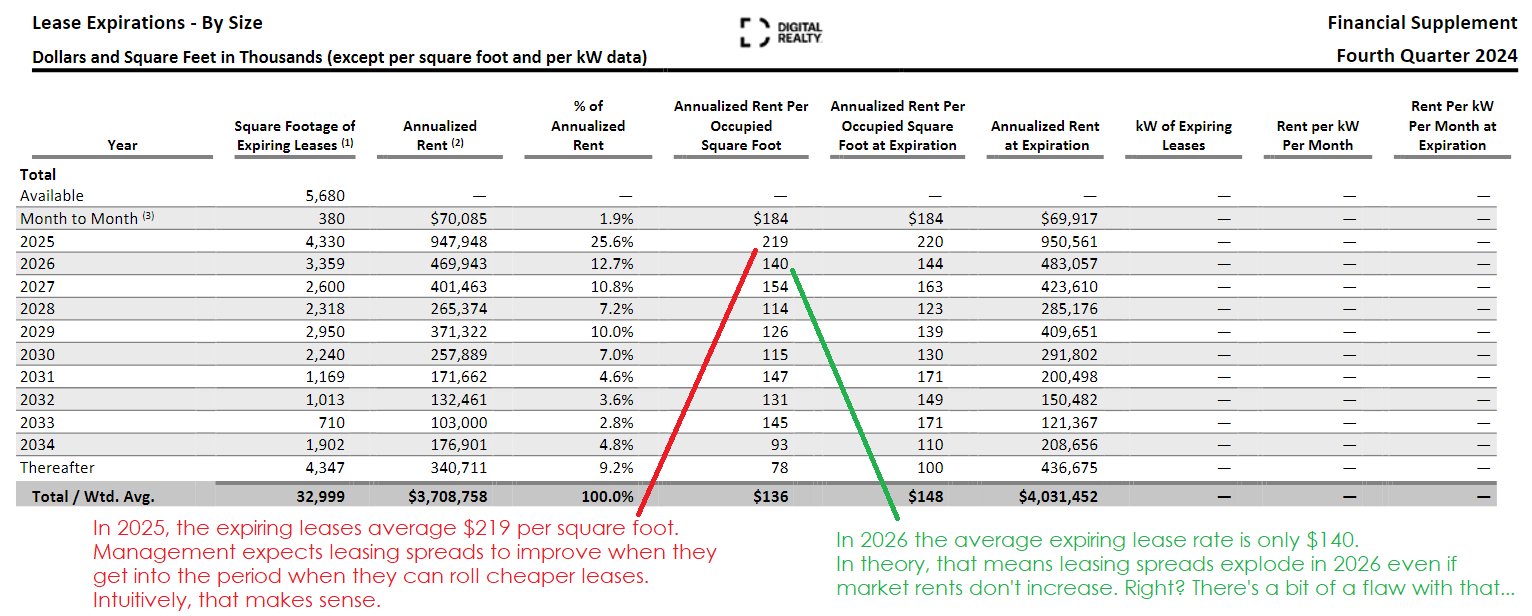

Well, we can pull the aggregate data on lease expirations by year to see if that makes sense:

Source: DLR, colored notes by author

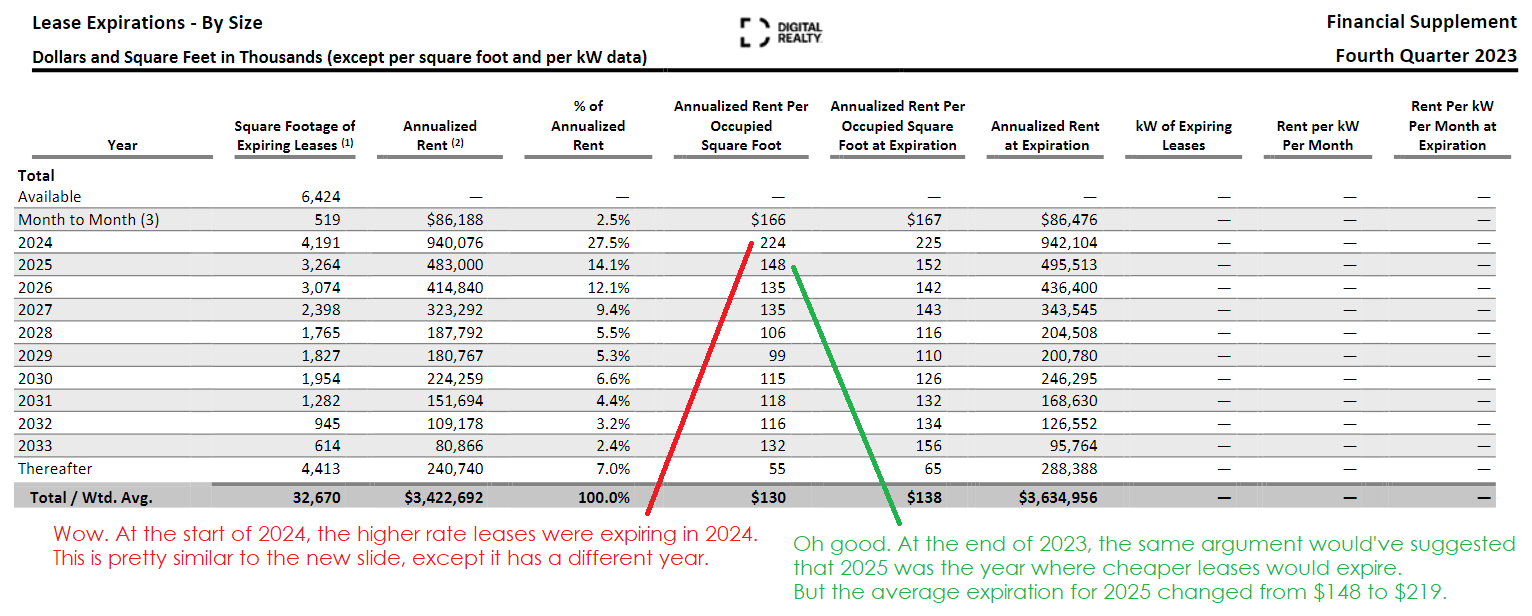

That argument looks really good on the surface. But we can put in a little more effort to backtest that theory. What if we pull the lease expirations from the Q4 2023 supplement? What did the picture look like one year ago?

Source: DLR, colored notes by author

I think that sums it up. When we get to 2026, the average lease expiration rate probably won’t be $140. It’ll probably be somewhere over $200 again.

What’s happening? Well, a significant portion of the leases DLR is signing have very short lease terms. Many leases that expired in 2024 were simply extended to 2025. It seems to me like that will probably happen again. So if leasing spreads really explode higher in 2026, it would be because market rents increased materially during the year. That would be very favorable for DLR. However, there’s an enormous amount of money going into data center development due to the massive yields.

Development Yields Drive Construction

The real money in data centers is the profits on development. It is not the operation of the assets. DLR’s pipeline is 70% pre-leased and the average expected yields are running at 12.1%. In the Americas the yields are even higher, reaching a staggering 13.7%.

What happens in real estate sectors when development yields become too attractive? New construction surges. In just the last few years:

- You’ve seen this with apartment buildings.

- You’ve seen this with industrial real estate.

- You’ve seen this with biotech labs (to an extreme).

The Future

I don’t claim to predict the future. I do make predictions about what is more or less likely to occur. That is simply a matter of reading the environment and evaluating what is more likely.

When the wind shifts, the excess new supply coming to market creates huge problems. While I find AI very useful, that doesn’t mean it is highly profitable today. The tech sector typically demonstrates some absurdly high operating margins. Margins that are not present for most AI products today. If prices increased to the level that would create typical margins for a tech company, I think the prices would drive many AI consumers out. Without massive consumption of AI services, how will demand keep pace with new construction? There’s also the risk of AI becoming more efficient. If AI becomes more efficient, it may take less data center capacity to handle any given job.

Finally, we have to consider the potential for a recession. Recessions are more probable at some points than others, but they are never impossible. Recessions are very bad for investment in new technology with minimal (or negative) near-term profits.

Conclusion

Digital Realty is guiding for much better growth in Core FFO per share. Not outstanding compared to other REITs. Very good (for this year), but not amazing.

Considering the tailwinds DLR gets from:

- Issuing shares and using the cash to buy Treasury Bills

- Developing properties at yields above 12%

- Low vacancy rates on a global level (despite DLR having high vacancy)

I don’t see this growth rate as particularly impressive.

Meanwhile, investors face the risk that any reduction in demand could lead to a scenario with excess supply that lingers for several years.

Digital Realty currently trades at $168.85. In my opinion, that price is still dramatically overvaluing the REIT. I have a very bearish view on Digital Realty due to the excessive valuation.

Member discussion