Digital Realty Achieves Insane Valuation

Digital Realty (DLR) reported their Q3 2024 results. We had a brief note in chat. This will still be pretty brief, but I want to touch on it further. How often do you hear me saying I want to touch DLR?

DLR’s results for Q3 2024 were better than Q2 2024, but that wasn’t a hard bar to clear.

The impressive achievement for DLR is getting their valuation so high.

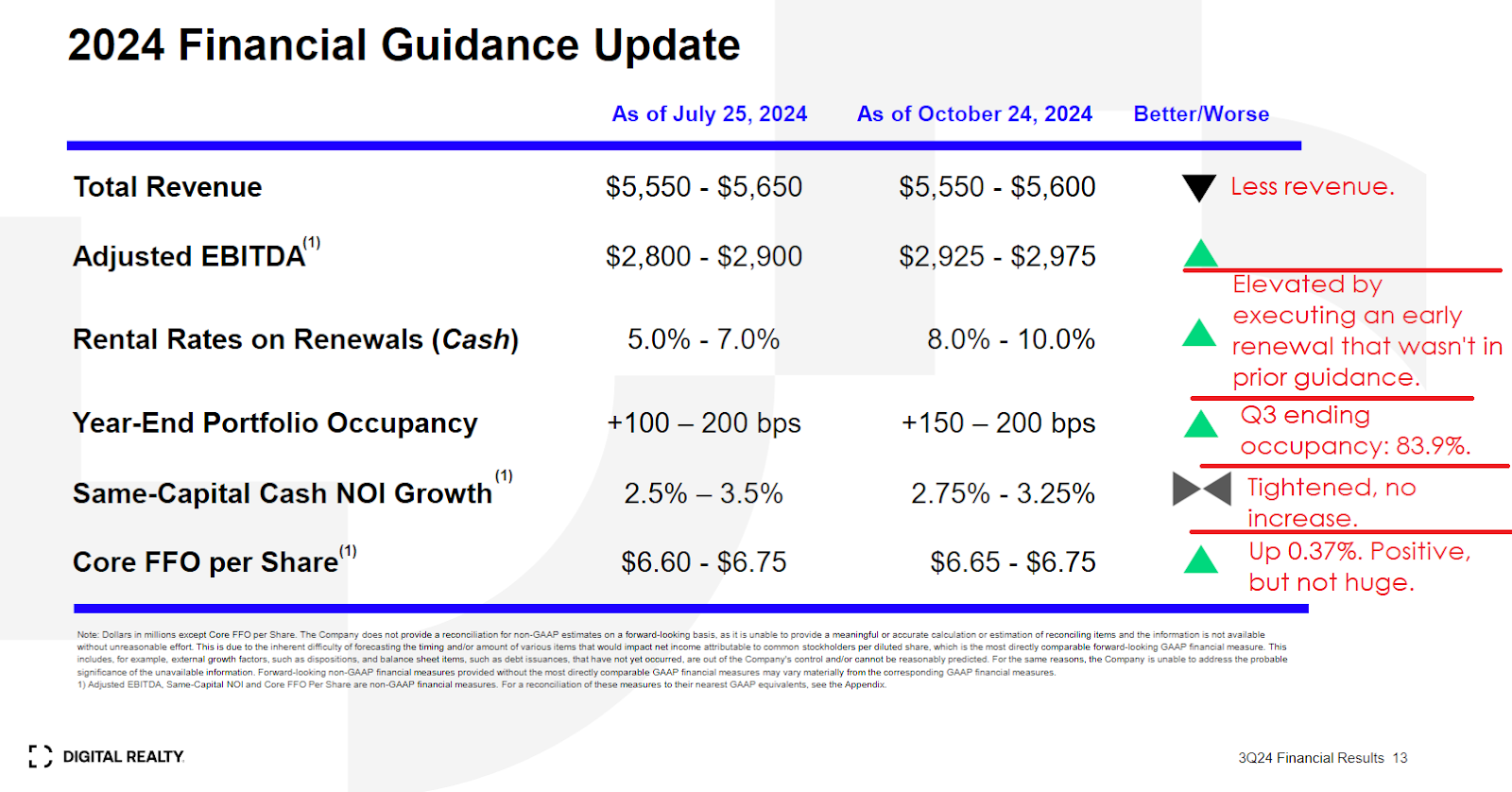

Digital Realty Guidance Update

I pulled the big slide DLR uses for updating guidance:

Sure, it’s an improvement. But barely. We need the historical context.

Digital Realty Historical Context

Let’s take a look at one of the tables DLR presented in their Q4 2019 earnings release:

Look at that Core FFO per share: $6.60 for 2018 and $6.65 for 2019.

Forgive me if guidance for $6.65 to $6.75 in 2024 doesn’t impress me. This isn’t a high dividend REIT. They weren’t paying out on a huge yield while creating painfully slow growth. A couple years of slow growth can happen, especially with rates ripping higher. But 6 years with minimal growth? If they hit the top end of guidance, they will be up 2.27% from 2018.

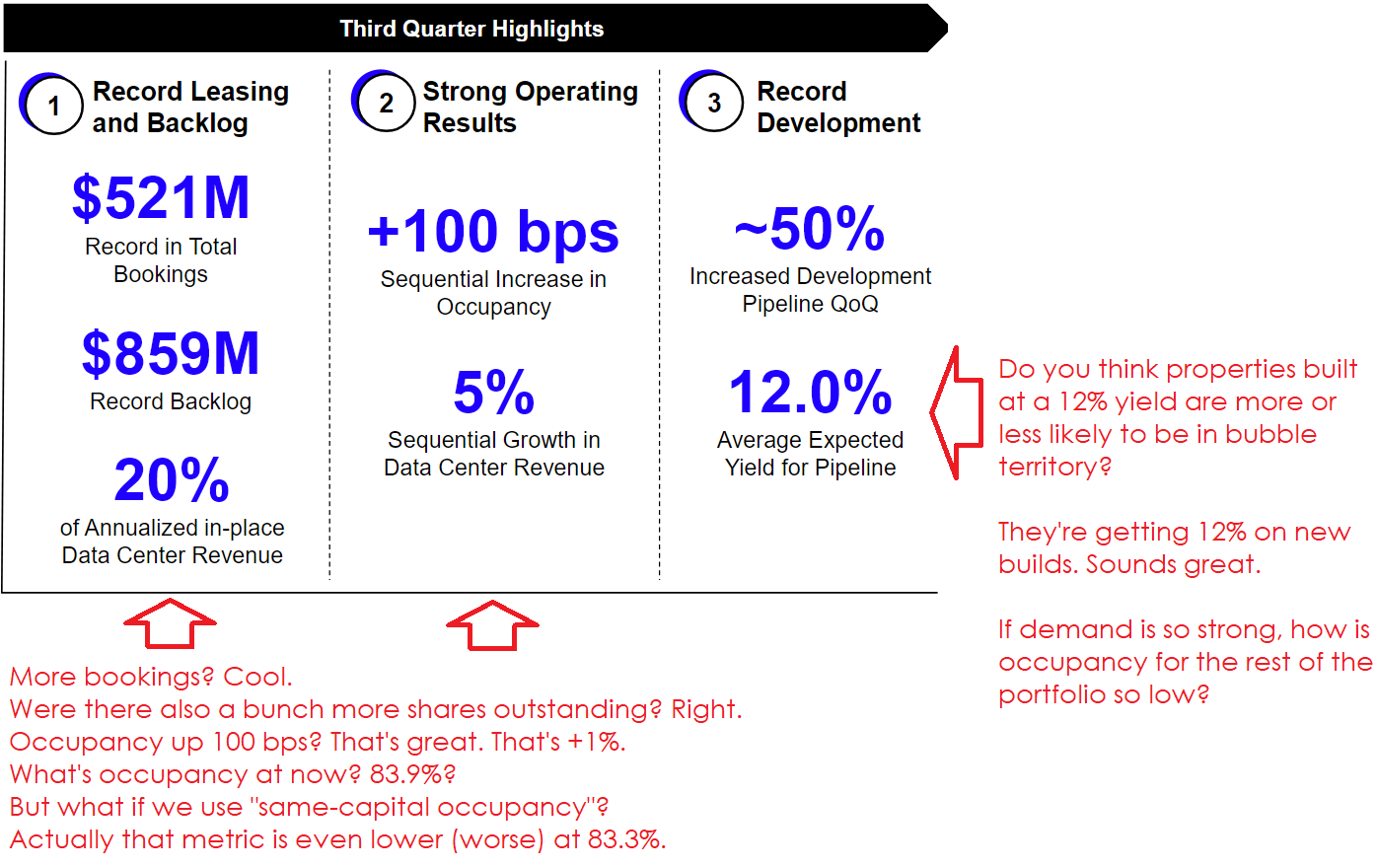

Digital Realty Highlights

These were the highlights from the quarter.

Look, that isn’t “bad’. If this REIT was trading at 10x AFFO, I’d be talking about the potential for this REIT.

But that isn’t the case. DLR trades at a staggering 28.4x AFFO estimates.

Do you think this real estate is worth 28x AFFO?

Which real estate?

Is it DLR’s old portfolio that could barely grow AFFO per share for 6 years while achieving about 16% vacancy?

Or is it the new stuff built at a 12% yield? Is real estate built at a 12% yield worth trading at a 3.52% AFFO yield?

Digital Realty Could Deleverage Accretively

With shares offering an AFFO yield of about 3.5%, DLR could issue shares, buy one-year Treasuries, and it would be a boost to AFFO per share. A REIT commanding a multiple above 25x should be providing massive growth. We should see properties leased dramatically below market rates. But cash leasing spreads were only projected at 5% to 7%. Normally a REIT trading at such a high multiple is going to post massive year-over-year growth.

Digital Realty Comparison

Let’s compare DLR to a REIT trading at 14.7x forward AFFO (Adjusted Funds From Operations). How about Alexandria Real Estate (ARE)?

- Alexandria Real Estate guided for 5% to 13% cash leasing spreads for the year.

- Alexandria Real Estate guided 3% to 5% cash same property NOI (Net Operating Income) growth.

- DLR guided for 8% to 10% cash leasing spreads including the significant positive impact of pulling a lease forward for early renewal.

- DLR guided for 2.75% to 3.25% cash same property NOI growth.

Now explain to me how Alexandria trades at 14.7x forward AFFO and DLR trades at over 28x forward AFFO.

I would encourage investors to look for any other REIT trading above 25x AFFO with such a poor history of growing AFFO per share. Good luck.

Digital Realty Outlook

I wouldn’t be surprised if DLR improves on their horrible record for growth. Realistically, it doesn’t take much to improve. Improving isn’t close to justifying a 28x multiple. That’s the burden for DLR over the next many years.

The best chance DLR has to create substantial growth is to issue a massive amount of equity at these inflated prices. That equity can be used to fund these development projects. They can also look to pay off their maturing debts by issuing more equity. It’s cheaper than debt and these share prices are like a gift from heaven for management.

However, the path to actually growing AFFO per share will take time.

Issuing shares to buy Treasuries would increase AFFO per share, but paying off debt will not. DLR’s debt had a weighted average rate of only 2.8%. That sounds very appealing, but the weighted-average years to maturity is only 4.7. They don’t get to keep the cheap debt all that long.

Conclusion

DLR is a perplexing REIT. The best chance the REIT has at growing AFFO per share is investing very heavily in development at huge yields. Incredibly attractive yields are attracting quite a bit of capital though. The market is betting on a staggering amount of growth. At this point, I think DLR would be wise to issue shares rapidly, even if they can’t find a use better than buying short-term Treasuries. They may eventually find some other acquisitions. When a low-growth REIT can print shares at 28x AFFO, there’s nothing better to do than print more shares.

The appeal of artificial intelligence is clear. Investors who can’t stomach buying those companies may look at REITs as an alternative way to play the space. However, DLR doesn’t have the same fundamentals as the AI companies. They don’t have huge barriers to entry. They can pretend to have huge barriers, but we know Prologis (PLD) saw the attractive profit margin on data centers and started developing them. They are the world’s largest industrial REIT. They are not a data center REIT. But they know how to develop assets profitability so they went to work.

I find DLR particularly unattractive. Even given acceleration in AFFO per share growth (from slightly over 0%), the multiple is absurd.

Disclosures: Long ARE, PLD. No position in DLR.

Member discussion