Demolishing an Awful Article on Invesco Mortgage Capital

Terrible articles get published. For better or worse, (mainly worse) it happens.

As the saying goes to ‘turn lemons into lemonade’, we can turn junk into articles into jokes. Why do such terrible articles exist? Well, there are a few reasons. One of the big ones is the “undercovered bonus” offered on Seeking Alpha. When there are not enough articles on a stock recently, authors can earn a bonus by writing about it. That can influence which companies an author decides to write on. Unfortunately, it’s possible to get that bonus without knowing much about the stock. This particular article on Invesco Mortgage Capital (IVR) was published when the bonus should’ve been $65. That’s enough for some authors to throw together whatever data they can find and call it “research”.

There is a silver lining though. Well, at least for us. I get to blast the article and you get to watch it get blown to bits.

Invesco Mortgage Capital Dividend Yield

At the time of writing, the dividend yield was about 18%. It is still about 18%.

Can Invesco Mortgage Capital support that yield? Temporarily, but not indefinitely.

The “analyst” believes that the yield has “potential for growth”.

I will admit that the yield might go up. If the price declines before a cut, then the yield would go up (until the cut).

IVR is only trading at a slight discount to our estimate of 09/30/2024 book value. We estimated the book value would be around $9.45. The $1.60 dividend rate represents a 17.7% yield on the share price of $9.05 or a 16.9% yield relative to our projected book value. But why does the dividend yield on book value matter at all?

Think about it simply. If you were managing a leveraged bond portfolio, do you think the income you could produce would be related to the amount of money you had available for investing? It’s not a trick question. The answer is obvious. Yes, your ability to produce income is related to the amount of money you are investing. If it wasn’t, you would invest $1, generate $100,000, and never work again.

That doesn’t work. Now we’re going to add in another figure.

I took the G&A (general and administrative) expenses and combined them with “management fee - related party”. The combined figures represent the overhead costs. For the last three years those expenses were:

- 2023: $19.73 million

- 2022: $25.32 million

- 2021: $29.23 million

Before you say that the numbers are trending in the right direction, you should understand that most of the change is coming from “management fees”. The reason those fees are declining is because the amount of equity available for investing is declining. For 2023, the combined overhead cost about 4% of the ending value for common shareholder’s equity.

Therefore, the common equity needs to be invested in such a way that after all leverage it is capable of earning a return of about 16.9% + 4% = 20.9%.

Part of the strategy involves having additional leverage from preferred shares. IVR has two series of preferred shares outstanding. Those two series combine to represent about 38% of IVR’s total equity (common plus preferred). That allows IVR to increase the effective leverage on common equity. However, you can still utilize this simple process to evaluate various high-yield investments:

- Can management consistently generate returns in excess of 20% before paying themselves?

- No.

If IVR’s management could do this, wouldn’t other mortgage REITs do it?

Adjusted for the massive reverse split, IVR’s quarterly dividend rate went as high as $10.00.

We can try to be more understanding. Instead of using the highest dividend rate, we can use the lowest quarterly dividend rate paid prior to the pandemic. That was $4.00 per share.

Today the quarterly dividend rate is $.40.

Given that information, do you believe management is about to shatter the mold and demonstrate how to consistently earn over 20% before paying themselves? Probably not. But you have an advantage. You’re not trying to throw together an article as quickly as possible to claim $65 plus a small amount of pageviews.

For reference, the biggest disaster was during the pandemic when IVR did not plan for the potential margin call scenarios effectively. They ended up having assets liquidated near the bottom in asset pricing.

Invesco Mortgage Capital Payout Ratio

The article got really special when it stated:

“Seen above, the company's GAAP earnings have been a loss for a few quarters, due mainly to unrealized losses on their investments. Yet, earnings available for distribution have been much higher than the dividend, giving a payout ratio of at least half. As the 90% payout ratio required by law for REITs is based on GAAP earnings, IVR has been able to retain value on its balance sheet for investment, rather than distribute it right away.”

Putting aside the language of “at least half”, we’re going to tackle the facts here.

Here are some facts:

- Earnings available for distribution is not a particularly reliable metric for dividend sustainability.

- The 90% payout ratio required by law for REITs is absolutely not based on GAAP earnings. That is just false.

- Whether IVR had an option to retain value or not, the fact is that they were distributing a massive dividend while book value per common share plunged.

Taxable Income

Walter Boudry, PhD teaches at the Stern School of Business. He knows quite a bit about REIT accounting. He even wrote a massive paper on REIT Dividend Payout Policy. In that paper he writes:

“First, I do not use GAAP financials to calculate taxable income. Instead I use the required tax disclosures from Form 1099-DIV to estimate taxable income. By starting with tax disclosures I am not prone to the same GAAP-to-tax differences that plague prior methods. Second, the payout rule I apply to my estimate of taxable income is determined by the payout requirements mandated in the Internal Revenue Code (IRC).”

You may notice some key terms there like:

- “I do not use GAAP financials to calculate taxable income”

- “I am not prone to the same GAAP-to-tax differences”

- “my estimate of taxable income is determined by the payout requirements mandated in the Internal Revenue Code”

I’ll openly admit that Walter Boudry knows more about REIT taxable income accounting than I do. Scott Kennedy handles any assessment of taxable income for the mortgage REITs we cover. Scott is great at it. I don’t need to deal with it. However, I certainly know enough to call someone out when they say the 90% requirement is based on GAAP earnings.

This reminds me of one of my favorite sayings:

“There’s nothing as helpful as factually inaccurate stock analysis prepared for a $65 bonus.”

GAAP Earning

It is just downhill from there.

The author proceeds to say:

“When the pendulum swings the other way, and unrealized losses no longer drag down GAAP earnings, IVR will be required to distribute more, and I believe this will result in a dividend increase, ceteris paribus.”

Was he quoting latin to sound smarter or to cast a spell from Harry Potter? My trick to sound smart is to spend more time doing research, but who doesn’t like a shortcut? My shortcut is to create a comparison between myself and that guy.

So what else is wrong?

Well, we could do something really crazy like:

- Pull up the dividend portion of IVR’s website.

- Load the dividend tax information from 2023.

- Load the dividend tax information from 2022.

- Load the dividend tax information from 2021.

If we did that, we would notice that none of IVR’s dividend for 2023 was marked as a return of capital. Just to verify that IVR knows how to fill out the form, we have the 2022 form showing a partial return of capital and 2021 showing a pure return of capital for common dividends. So will a swing in GAAP earnings be a big factor to drive dividends higher? No.

Net Interest Margin

The author thought a dividend increase would be supported by an increase in their net interest margin.

That was stupid. I’ll demonstrate why.

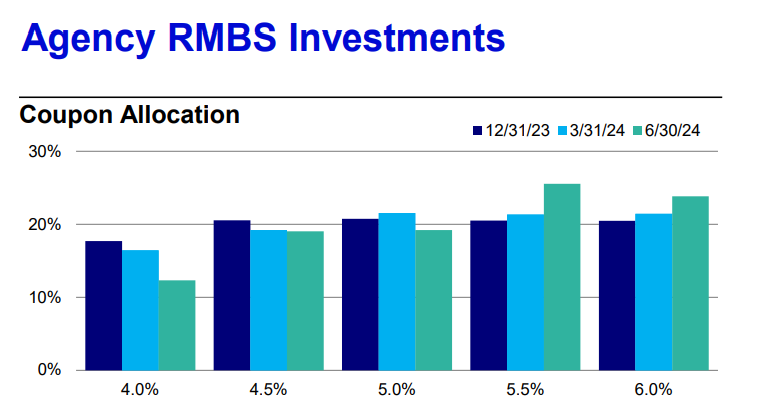

These are the fixed-rate agency RMBS that represent most of IVR’s assets:

What’s the average rate across those?

A bit over 5% right? Therefore, the yield will probably be around 5%.

Here’s confirmation:

Notice how the yield is a bit over 5%? Great They are earning a bit over 5%. Now about 5.48%.

You may also notice that the repo rate was very similar to the yield on agency RMBS.

The analyst actually noticed that the weighted average rate on repurchase agreements (the primary source of debt) was running at 5.46% in Q2 2024. That’s great. But if IVR has assets that yield 5.48% and finances them at 5.46%, they are not earning much on the spread.

But IVR is reporting enormous “earnings available for distribution”. So what gives?

Notice the dark blue bar at the bottom. That’s the rate IVR is paying on their swaps. IVR has a hedge portfolio that covers the vast majority of their borrowing. That hedge portfolio is essentially holding the cost of funds just slightly over 1% even. Because IVR already covered most of their repurchase agreements with long-term hedges, they have minimal exposure to the change in the rate on repurchase agreements.

That’s why IVR was able to report such absurdly high earnings.

We can compare the net interest margin with and without swaps:

See, it would only be 0.02% without the swaps. But with the swaps it was 4.09%.

The author assumes that lower rates will reduce the rate IVR pays on their repurchase agreements.

That’s true. But the total borrowings were $4,260 million and the swaps covered $3,915 million of it. That’s 91.9%.

So would the swaps offset “some” of the savings from a lower rate on repurchase agreements or “about 91.9% of the savings”?

Terrible Analysis on Invesco Mortgage Capital

The author later compares price to trailing book value. That’s useful for analysts who don’t have access to current estimates. That’s fine. It’s not great, but it’s something. It ignores that book value was generally declining during many quarters over the last few years. That means the book value on any given day was often less than the book value from the prior quarter (throwing off the ratio), but at least there was some effort.

Unfortunately, that effort was undercut by those pesky things called “facts”.

The article says:

“It's worth reminding folks that, with a higher-coupon portfolio, rate cuts tend to make such assets increase in market value, and this can contribute to a rise in tangible book.”

The problem here is that it says “with a higher-coupon portfolio”.

When interest rates decline, all fixed-rate MBS generally increase in value. Which ones increase the least? The ones with higher coupons. Why? Because they are more likely to be prepaid. Prepayments happen 3 ways:

- The homeowner makes an extra payment.

- The homeowner sells the house and therefore pays off the mortgage.

- The homeowner refinances.

The big one is the third one. If you had a mortgage with a 6% coupon rate:

- You might be interested in refinancing at 5%.

- You would definitely be interested in refinancing at 4%.

If you had a 4% coupon rate, you probably wouldn’t refinance to 4%. It would be a huge waste of your time.

Consequently, higher rate mortgages always have a higher risk of being prepaid. Since Invesco Mortgage Capital owns the MBS, they don’t want it to be prepaid if rates fall. Therefore, if rates are going down, the higher-coupon MBS see a smaller increase in value.

On one hand, the author tried to include book value. On the other, the author was wrong about how asset values react to a change in interest rates.

That earns a participation trophy:

Conclusion

The article ends by referencing higher margins as “rate hikes” are implemented. At this point, I don’t care to explain the difference between rate hikes and rate cuts. As you might imagine, the author did not spend any portion of his $65 bonus on buying shares of IVR to back up his bullish view.

Disclosure: I am not invested in IVR in any form. I did not get a $65 bonus for this article.

Member discussion