CPT Q3 2024 Earnings Update

Summary

- Respectable beat on AFFO and Core FFO per share.

- Guidance slightly increased for Core FFO per share.

- Guidance for same store NOI flat.

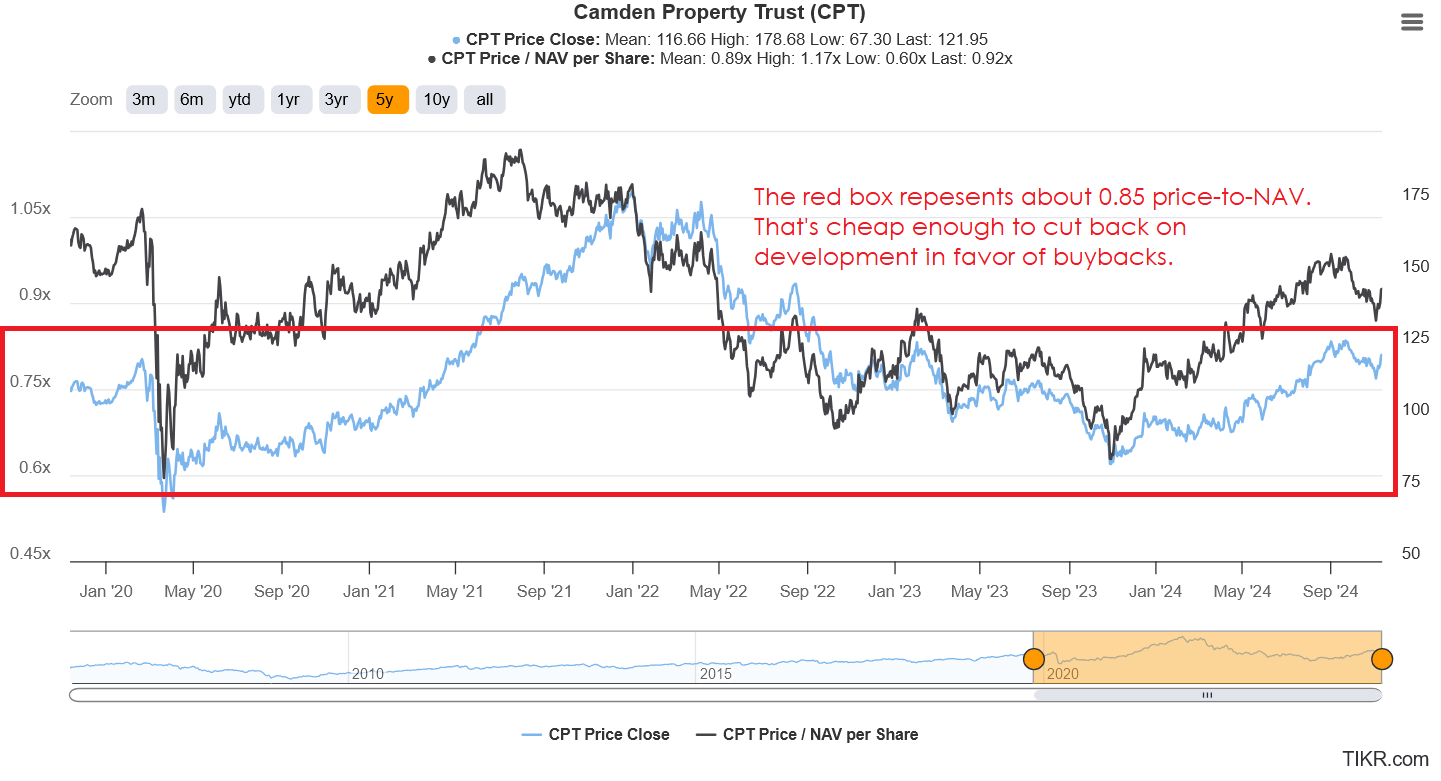

- Discount to NAV has declined substantially as prices rallied.

- Multi-family starts have plunged. Completions will follow. We’ve highlighted this for a long time.

- Camden Property Trust (CPT) highlights upcoming multi-family maturities as potential opportunity to find a few more deals on apartment buildings.

- Fundamentals all look good. Targets may decline moderately due to the surge in Treasury yields. CPT currently in neutral range.

- I’m sitting on a huge capital gain for my position purchased on 11/16/2023 at $88.23. I may consider reallocating part of that position after it hits long-term capital gains (depending on valuations for CPT and for other REITs). Up over 40% including dividends.

- After we finish the apartment REIT updates, we’ll have target updates on the sector.

Camden Property Trust Results for AFFO Per Share

- Consensus estimate: $1.43

- Actual: $1.48

- Result: Beats by $.05

Great result.

Camden Property Trust Results for Core FFO Per Share

- Consensus estimate: $1.67

- Actual: $1.71

- Result: Beats by $.04

Great performance again.

Camden Property Trust Guidance for Core FFO

- Old guidance: $6.79

- New guidance: $6.81 (range $6.79 to $6.83)

- Change: Up $.02.

- Consensus $6.78

- Difference vs. Consensus: Up $.03 above consensus.

It’s not a huge change, but it’s positive. Looks good.

Camden Property Trust Guidance for FFO

- Old guidance: $6.72

- New guidance: $6.69

- Change: Down $.03.

Doesn’t really matter because Core FFO guidance is up and calculations for Core FFO are superior.

Same Store Net Operating Income for Camden Property Trust

Projected revenue and expenses were both slightly reduced. Net impact is neutral to NOI (Net Operating Income):

Net impact on NOI is neutral. No big deal.

Anything else significant should be from the earnings call.

Developing Apartment Communities

Camden Property Trust develops many of their own properties. I’ve criticized apartment REITs for development projects when shares trade at a significant discount to NAV (Net Asset Value).

The discount to NAV is materially smaller today:

Shares delivered over 40% (including dividends) over the last year. A year ago, many investors claimed apartment REITs were uninvestable because of poor leasing performance amid surging supply. When a good company is “uninvestable”, that’s often the best time for investing. It is always darkest before dawn. The trick is just to avoid buying trash like Medical Properties Trust (MPW). Eventually, the good companies bounce back. The narrative changes.

- November 2023: New supply is getting even worse. Spreads are going to be horrible. All apartments are trash (purchased shares at $88.23).

- November 2024: New supply is peaking! The supply picture will just keep getting better. Woo! (Shares are $123.42).

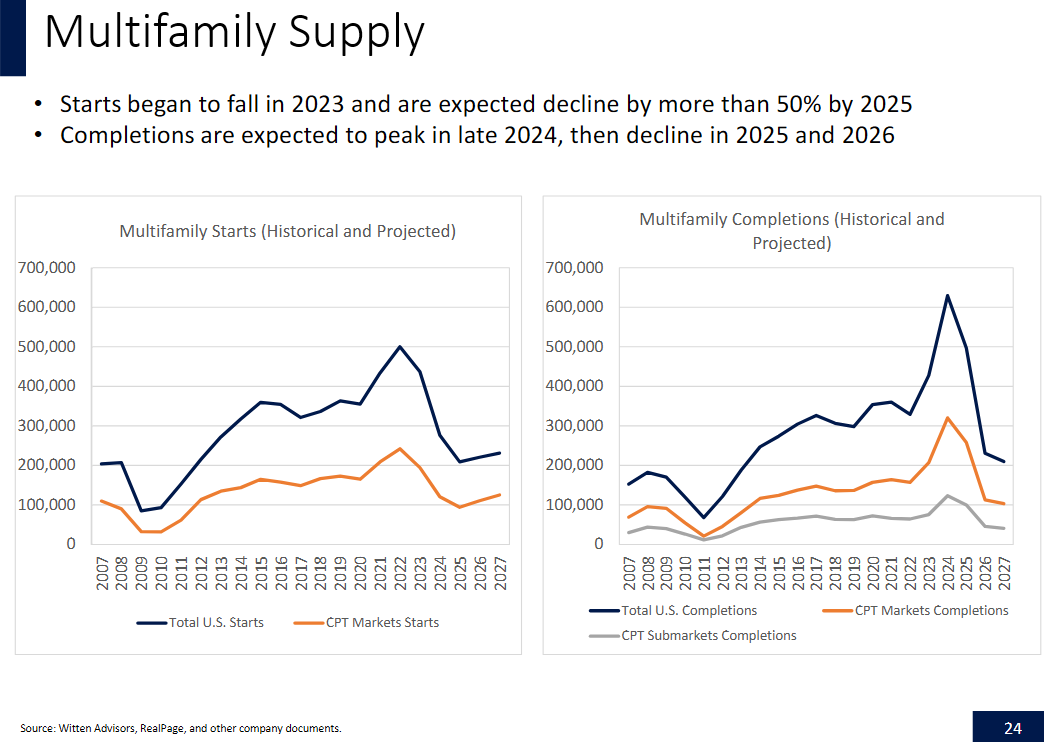

Multifamily Starts and Completions

This is a slide Camden Property Trust provides occasionally, though it shows up in mid-quarter presentations rather the earnings update:

Note: The term “starts” indicates the start of construction for new apartment units. So 500,000 meant projects for 500,000 apartment units were started.

That’s the historic surge seen in starts and competitions, along the much lower level of starts expected soon. Starts are expected to come in lower than they have since about 2013.

Evaluating the Earnings Call for Camden Property Trust

I went over the Q3 2024 CPT earnings call transcript.

From opening comments:

“New apartment supply is at an all-time high, 50-year peak, as we all know. And while absorption has been great, filling these apartments has limited meaningful rent growth in most of our markets. Trailing 12-month starts are off 35% with monthly starts off 49% from the highs. This backdrop should put new multifamily starts in the mid-200,000 range next year.

Witten Advisers projects rents bottoming out in 2024 and through the first half of '25 and then starting to accelerate to '26 and '27. We look forward to sharing additional details on our strategic plan and future market concentration goals along with our 2025 guidance when we report fourth quarter and full results next year.”

In our commentary on apartment REITs, we’ve regularly referenced the current surge in completions and the dramatic reduction in completions coming up over the next several years.

Another interesting comment about the multi-family debts coming due:

“We think 2025 and '26 is going to be a really interesting year, a couple of years. You have $650 billion worth of multifamily debt coming due. You have merchant builders who have prefs that are eating into their profits. Banks who want their loans paid down.”

CPT is talking about the right strategy. Going into that market to bid for assets. CPT doesn’t need to build their own apartments. They can save their capital. Talk to the lenders about foreclosing on the failing developers and immediately selling the property to the apartment REIT. Whether the project is complete or in process, CPT has the expertise to turn into a productive asset.

Later in the call, management said:

“When you look out at the projections out there, I mean, Wit associates has markets like most of our markets growing at 4% to 6% in '26 and '27. So theoretically, if you had to build, you could do a pro forma that showed outsized rent growth in the second, third, fourth, fifth years that could get those IRRs to work. The challenge that we have is we just don't want to push the edge of the envelope that hard today. We don't have to build and we would rather deploy the capital in markets we want to grow in, and buy existing properties at below replacement cost that don't have the lease-up risk.”

Management is also still looking at buybacks, as they discussed the implied cap rates:

“And I guess one of the – when you think about capital allocation, we – if stock prices get to the point where they were when we bought $50 million of shares at $97, at today's stock price, it's pushing up on a 6% cap rate. And it's hard for me to find is going in 6% that's existing today or a development going in 6%. So if the public markets don't believe the private markets that cap rates are 4.5%, we can buy our stock at 6%, you can expect more of that.”

Two other highlights:

- CPT is forecasting long-term compound growth rates for their apartment rents around 3% to 3.5%.

- Projections from a third party suggesting 4% to 6% rental rate growth in many of CPT’s markets in 2026 and 2027.

Why Lenders Should Talk to Camden Property Trust

The lenders would be wise to listen to such offers because it would provide a rapid solution. CPT isn’t bailing the lender out. CPT knows they have a strong position, so they don’t have to bid high. The lender may take a loss on the loan, but it would significantly improve their position for negotiating with other deadbeat developers. The correct solution is to just foreclose. Eat the loss. Hold it up as an example to the other borrowers. Default on a loan and lose the entire equity position. Too many lenders are extending credit to bad borrowers, which only emboldens the rest of them to behave worse.

That’s the problem when lenders only look at one loan in isolation. For a single loan, the best solution (net present value) is usually to extend and negotiate. However, that becomes a problem for the lender when other borrowers decide they can negotiate for a better deal. The lenders don’t like the legal costs, carrying costs, and so on. Well, if you were that lender, wouldn’t you be interested in talking to a potential buyer like CPT?

Conclusion

The earnings release for CPT was pretty good. Nothing wild, but nothing to dislike in the fundamentals.

The only negative for CPT recently has been the increase in medium-term and long-term Treasury yields. Those higher Treasury yields can weigh on valuations for most REITs, though apartment REITs aren’t down as much as some other sectors. So good fundamentals are being offset or partially offset by Treasury yields.

CPT currently trades in our neutral range. Based on the swing in Treasury yields, I expect a moderate reduction in targets during the next update.

We did the prior set of target updates for apartment REITs in Q3 2024. When we set the targets:

- The 5-year Treasury was 3.759%. Today it is 4.280%.

- The 10-year Treasury was 3.885%. Today it is 4.420%.

- Both rates were trending lower rapidly. Today, both are firmly trending higher.

That’s the only thing I see weighing on CPT presently. The impact of the higher rates may be partially mitigated by the upcoming period of reduced supply leading to a stronger leasing environment.

After my purchase from 11/16/2023 hits long-term capital gains, I might reduce it depending on valuations throughout the sector.

Disclosure: Long CPT.

Member discussion