AvalonBay Communities Vs. Rexford Industrial

By Michael VanLoon, AKA Colorado Wealth Management Fund

AvalonBay Communities (AVB) vs. Rexford Industrial (REXR) is an interesting comparison.

In AvalonBay, we have a national apartment REIT with a focus on coastal markets (especially bigger cities). They are expanding a bit into sunbelt markets, but it’s mostly coastal.

In Rexford, we have a Southern California industrial REIT.

Both REITs have some expertise in development and redevelopment and view their development programs as a way to enhance shareholder value.

Comparing apartment REITs with industrial REITs is inherently a bit strange. However, that can make it more intriguing for the reader.

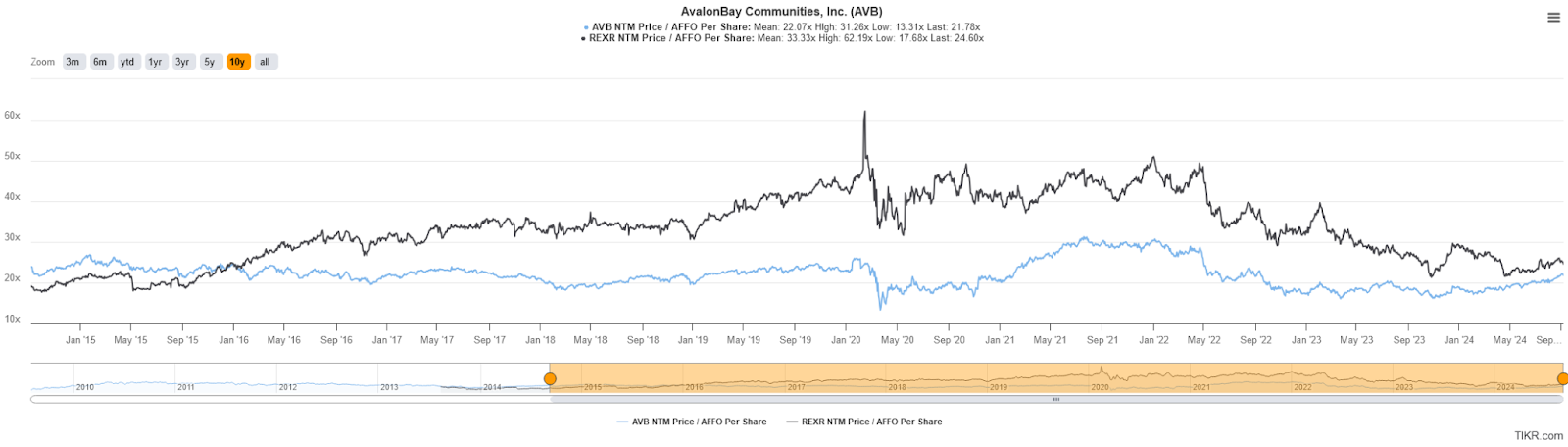

Charts

The first step is valuation:

- AVB trades at about 22x forward consensus AFFO estimates.

- REXR trades at about 25x forward consensus AFFO estimates.

That makes it sound like REXR is more expensive, but the historical multiples tell a different story:

This first chart demonstrates the historical gap in forward AFFO multiples:

Source: TIKR.com

You can tell that the gap in AFFO multiples today is near the smallest it has been since early 2016.

On average, REXR’s leases are still significantly below market; they are much further below market than AVB’s leases.

However, AVB does benefit from the shorter duration of their leases allowing them to raise rents on almost all of their customers within a year.

Looking at that chart might lead investors to think that buying the one at a lower multiple was always the better strategy.

That’s wrong.

You can tell REXR’s multiple was higher throughout 2017, 2018, and all the subsequent periods. By summer 2019, the multiple for REXR was materially higher.

Yet if an investor was buying one of these REITs, turning on dividend reinvestment, and logging out for many years, the investor buying REXR would’ve won for many periods.

If the purchase was before August 2019, then the investment in REXR outperformed (using today as the end date). Despite a much higher multiple, REXR delivered such massive growth in AFFO per share that it overcame the gap in multiples.

However, if the investor bought after roughly the middle of August 2019, then AVB had stronger returns from the vast majority of start dates.

So it isn’t simply a matter of picking the REIT with the lower AFFO multiple.

It is absolutely never a matter of picking the REIT with the lowest AFFO multiple.

Lowest AFFO Multiple

That’s how you get Medical Properties Trust (MPW). That’s how you get Washington Prime Group (WPG) or CBL Properties (CBL). Those were all publicly traded REITs at one point. MPW is still publicly traded. CBL is publicly traded again. CBL did declare bankruptcy, but they are back and that’s about it.

Don’t even think about asking whether CBL has been a great investment since it started trading again. You know the answer intuitively.

It’s not even about the real estate. Yeah, obviously low-quality malls are awful.

Did you know Stephen D. Lebovitz was the CEO who oversaw the value of CBL common shares going from quite a bit to nothing?

How well were shareholders represented when the value of a $1 million investment declined to less than the price of a small fry?

Hope they weren’t reinvesting their dividends!

Yes, the pandemic made things worse. But CBL was in a horrible position before 2020 began.

Why does that matter? Well, after giving shareholders basically the worst possible outcome, CBL emerged from bankruptcy and still has the same CEO!

The reward for shareholders losing everything was that the board of directors, who is bound to act as fiduciaries, decided to keep the guy who utterly failed to avoid a complete loss.

Who's more qualified than a guy who oversees the worst possible outcome even after analysts warn him explicitly on the earnings call?

How about that homeless guy you passed on the street? Odds are he didn’t drive any companies into bankruptcy.

Why couldn’t the board hire him?

CBL filed for bankruptcy on November 1st, 2020.

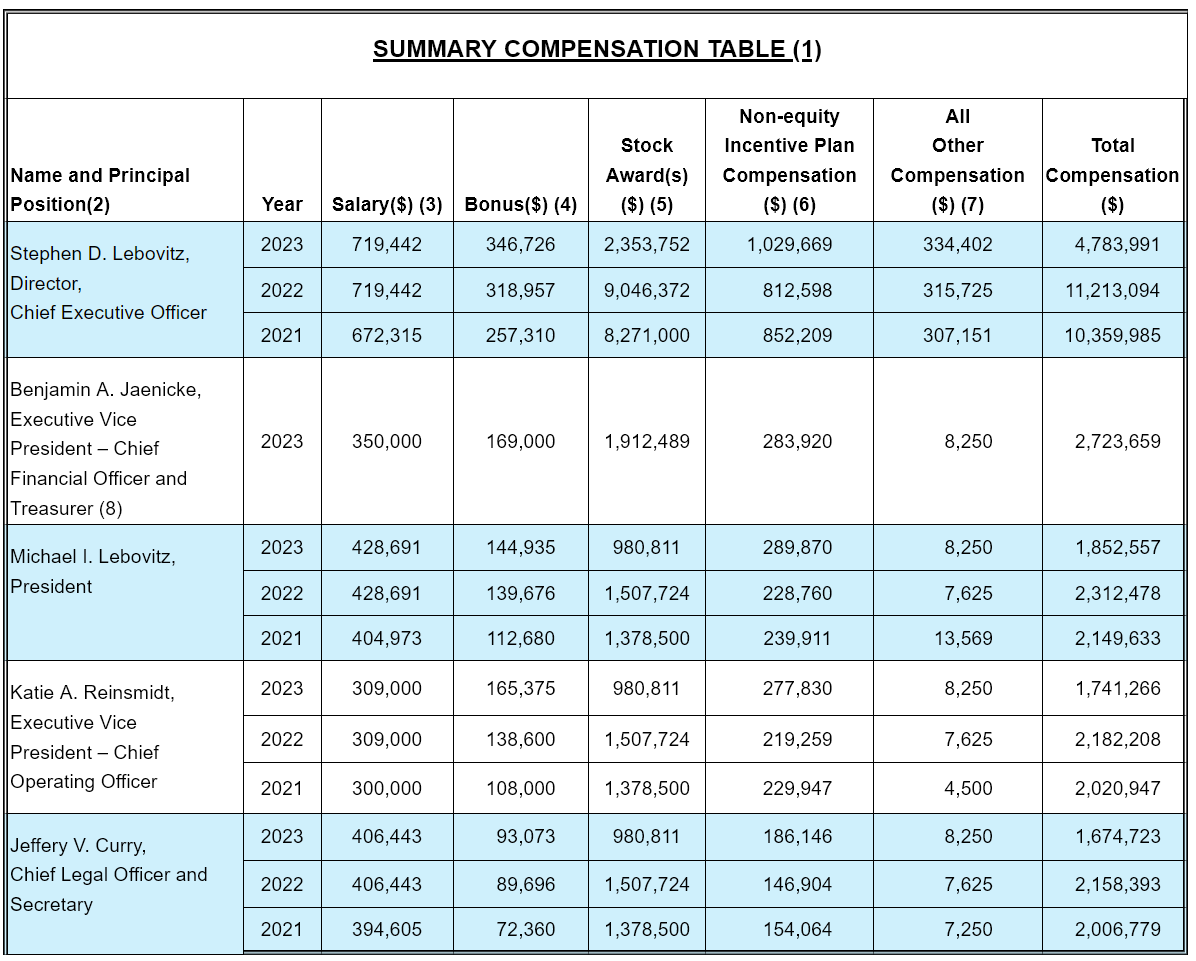

During 2021, 2022, and 2023 combined Stephen D. Lebovitz collected total compensation of $26.357 million:

Source: CBL Filing with SEC

Meritocracy is dead.

This wasn’t the death blow. This is just one of the parties on the grave.

I bet the board didn’t even try offering the homeless man $26 million over 3 years to see if he would do the job.

They just settled for the warm body that was already in the seat.

Gotta give it up for the complacent shareholders as well.

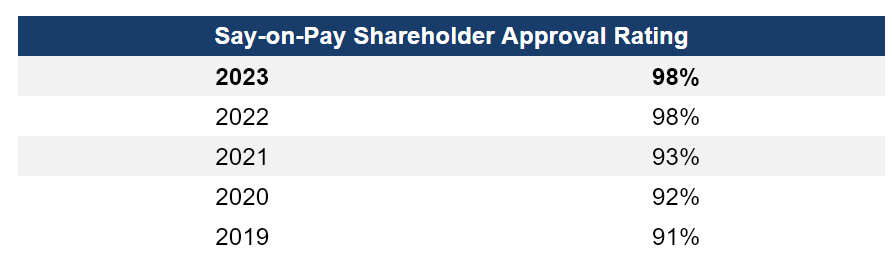

In 2022 and 2023, CBL’s “say-on-pay” advisory vote had 98% support.

Who voted in support of this?

Well, these are the kind of people who saw what happened to the mall REITs and thought:

“Man, I really wish I could own the worst properties with some of the worst management. This time it’s going to be a winner.”

Returning to The Article

At this point, it should be clear that:

- A low AFFO multiple alone is not enough to warrant a bullish outlook.

- When comparing multiple REITs, the REIT with the lower multiple is not necessarily a better investment.

- The AFFO multiples over time can be one useful data point to consider.

- The expected growth rate for AFFO per share is also very important.

The Impact of Rates

Lower rates should be more useful for Rexford than for many of the apartment REITs.

If Rexford grows their total portfolio faster (acquisitions + developments), then it will issue more new debt relative to existing debt.

Consequently, lower interest rates are more important for the weighted average cost of debt.

There’s one quick and dirty way to ballpark the rate of acquisitions for a REIT.

This technique works best if you’re comparing high-quality REITs with roughly similar dividend payout ratios and without drastic changes in leverage.

AVB and REXR are both high-quality REITs. The payout ratio for REXR is a bit higher, but the difference isn’t big enough to be a problem. Leverage has changed modestly, but certainly not drastically.

Consequently, investors can use the growth in shares outstanding to get a rough feel for how quickly the REIT is growing its portfolio.

There are times when investors should be very precise here, but in this case, the gap is pretty obvious:

Comparing 2023 with 2016:

- AVB’s weighted average diluted shares outstanding barely increased.

- REXR’s weighted average diluted shares outstanding more than tripled.

Therefore, REXR has a vastly larger emphasis on acquisitions.

You could also look at the amount spent each year on acquisitions minus dispositions, but this technique is much faster and reaches a very similar result.

Accretive Impact to AFFO

If acquisitions are partially funded by debt, then a lower interest rate can make the acquisitions more accretive.

Making acquisitions more accretive enhances FFO and AFFO per share growth rates for REITs who are using acquisitions effectively.

Since AVB is not aggressively issuing equity and debt, the benefit for AVB from lower interest rates is smaller than the benefit for REXR.

However, there’s one more factor.

Lower interest rates make buying a home cheaper.

Due to the increase in home prices and interest rates, very few renters could afford to buy a home over the last two years.

If interest rates fall, the monthly cost of home ownership will decline. That gives renters more flexibility in their choices.

That is a modest headwind for apartment REITs, though it should have a much smaller impact than the change in new supply.

For industrial REITs, that headwind doesn’t exist. There isn’t a huge market of other properties that many tenants wish they could purchase.

Consequently, apartment REITs should get a smaller benefit from lower interest rates than industrial REITs.

The Impact of Supply

Both apartment REITs and industrial REITs have been facing excess supply in 2024.

Both types should see a reduction in supply during 2025 leading to dramatically lower new supply in 2026 and probably 2027.

That should be a favorable background for pricing new leases.

We’ve expected this for the last few years, but the market still sold off REITS pretty hard.

The Impact of Demand

There is a long-term shift towards e-commerce. It was accelerated during the pandemic but weakened a bit afterward.

E-commerce typically takes around 3 times as much space per dollar of sales.

Why? You can’t store the product on the store shelf when your store is digital. If you’re selling in WalMart, you have a bunch of inventory inside the WalMart store.

The product that a customer might purchase in the next 30 minutes is the product on the store shelf. But if you’re selling online, the product a customer might purchase is still inside an industrial property.

Further, industrial real estate is still vastly cheaper per square foot than retail. Since that space is cheaper, it tilts the math in favor of using more space to avoid running out of stock.

If someone suggests industrial rents would rise to the level of retail rents, they would be making an extreme bull case for industrial real estate.

I won’t make that argument, but I will suggest that industrial rents will probably resume trending higher within the next few years.

Looking at REXR, it’s interesting to note that the Southern California industrial market (the hottest in the world for a long time), has seen more weakness than several other areas. We’ve heard about that from the management of multiple industrial REITs.

California

Looking at Essex Property Trust (ESS), we see strength in California.

Note: The ESS owns apartment buildings in California and Seattle.

ESS has raised guidance twice already in 2024 and the increases were material. As we predicted quite some time ago, the stories about the demise of California were overstated. They’ve also seen a resurgence in the share price.

However, we want to focus on the implications for REXR.

Demand for REXR can be complicated. The Southern California industrial market delivers to Southern California, but it also handles products delivered throughout much of the United States. For people who aren’t familiar with geography, California benefits from ocean access to China. It is easier to ship goods from China to California than to other parts of the country. That’s how continents and oceans work.

I want to emphasize the local delivery though, because there is no alternative to Southern California industrial real estate when a company is selling to customers in that region.

Land in California

Land in California is expensive. They have great weather, great beaches, and terrible zoning. Sorry for anyone who likes California’s zoning laws.

Some big cities in California are stuck with an excessive amount of office real estate.

Some local governments may fight efforts to replace office real estate with better uses.

Those governments will be sentencing their cities to more traffic and higher taxes.

The correct solution is to permit office real estate to be redeveloped into residential. Of course, most office real estate won’t be good candidates. However, redeveloping 10% to 15% could still have a material impact.

What about redeveloping office properties into industrial properties? That’s not likely to happen because:

- The office buildings are usually very tall. Industrial real estate is not tall.

- Industrial real estate usually has a much lower value for the building relative to the land. Building industrial real estate in the CBD (central business district) wouldn’t be optimal.

- Industrial properties need additional space and road infrastructure for backing up huge trucks. That won’t work for the road infrastructure.

Consequently, we don’t have to worry about office properties turning into industrial real estate.

Scenarios

There are three scenarios:

- No office to residential. Seems unlikely since some projects are already underway across the country.

- Some office to residential. Seems extremely likely.

- Massive conversions from office to residential. Seems unlikely since many office buildings are a poor fit for conversion.

Since scenario 2 is vastly more likely than the others (my projection), we can use that as our baseline.

Any office-to-residential conversion is a slight negative for apartment landlords (new supply), but it is a tailwind for industrial REITs.

All else equal, industrial REITs want to see higher population density around their properties. It drives up rent because the property is more useful for local deliveries.

That’s why some industrial REITs will include charts comparing the average population density around their properties compared to the population density for peers.

Further, population density tends to drive up real estate prices. Higher real estate prices create additional barriers to new industrial supply.

The long-term thesis for industrial rent growth is based on the supply-demand dynamic.

The industrial REITs don’t need these conversions to happen. It is simply a source of bonus upside that the market seems to be ignoring.

Conclusion

We’ve seen the AFFO multiples tightening substantially between apartment REITs and industrial REITs.

The apartment REITs stand to benefit from less supply, but that tailwind may reach the industrial REITs as well.

Given the tighter spread in multiple, I’m inclined to favor the industrial sector.

Over the next decade or two, I would expect more growth in industrial rents than residential rents.

As it stands today, most industrial REITs have below-market rents in place on many existing properties. That gives them an additional tailwind. However, since they only roll over a small portion of leases each year, it takes longer to recognize the benefits of higher revenues.

I picked REXR over Terreno (TRNO) and Prologis (PLD) at this point based on valuation. REXR's price has been struggling more. I attribute the weaker price performance primarily to the headwinds for Southern California industrial real estate over the last 1 to 2 years. However, we have significant positions in all 3. Before our most recent purchase of REXR, our REXR position was smaller than our TRNO and PLD positions.

Disclosure: Long REXR, TRNO, PLD.

Member discussion