Agree Realty Q4 2024 Earnings Update: Another Solid Quarter

Summary:

- Agree Realty (ADC) beat consensus estimates for AFFO by $.01.

- Guidance is reasonable and management’s commentary suggests the guidance may be a little bit conservative.

- Guidance calls for about $1.2 billion in acquisitions. Due to the favorable cost of capital, these should be accretive.

- Historically, ADC has demonstrated a pretty stable growth rate for AFFO per share.

- The run higher in Treasury yields is a headwind for all of the REITs.

- We’re forecasting a slight reduction in targets as the impact of Treasury yields on price targets outweighs another solid quarter.

Agree Realty recently reported Q4 2024 earnings.

Earnings Results

- Q4 2024 Core FFO: $1.02 (matches consensus)

- Q4 2024 Management AFFO: $1.04 (beat consensus by $.01)

- Full Year 2024 Management AFFO: $4.14

Note: There are some incorrect headlines, as shown below:

Guidance for 2025

- Management AFFO guidance: $4.26 to $4.30 (midpoint $4.28)

- Guidance implies 3.38% growth (rounding to nearest penny).

- On the earnings call, management indicated that the guidance may be on the low side.

Issuing Shares

As a net lease REIT, ADC’s strategy involves issuing new shares to fund external growth. This growth is usually accretive to their “per share” metrics, which are the ones shareholders should care about. After all, you want to know how much money the company is generating for you.

ADC used a forward equity offering during Q4 to lock in the price for another 5.06 million shares. Total net proceeds are projected at $368 million. That leads to $72.74 per share (rounded).

Is that a good plan?

Yes. ADC is selling the shares at a valuation where they are getting enough cash that their acquisitions (new real estate) should more than offset the increase in shares.

Forward Equity Offerings

Using forward equity offerings is simply a way for the REIT to proactively lock in the price on issuing shares. They already know the valuation for the properties they are considering buying. They use the “forward equity offering” to lock in the price for issuing shares.That makes it easier for the REIT to negotiate to purchase additional properties since they know how many shares they are issuing to fund the transaction.

In total ADC has about $900 million in future net proceeds for issuing shares. These shares don’t exist yet, but the price is fixed so this counts towards liquidity.

Why not issue the shares in advance and then sit on cash? One reason is that it makes the financial statements harder to analyze. It’s ideal if the share count increases at precisely the same time as the properties are acquired. This method allows the REIT to put those dates much closer to each other.

Note: There are some complications with accounting and the “treasury stock method”. Guidance is already factoring in that these accounting rules may reduce 2025 AFFO per share by about $.01 to $.02. This isn’t big enough to be worth worrying about, but as an analyst it’s nice to see management address it proactively.

Acquisitions

During Q4 2024, Agree Realty acquired another 98 properties for a total price of $341.5 million at a 7.3% cap rate. That’s pretty similar to the amount of future net proceeds from their forward equity offering. Typically the net lease REITs will fund around 25% to 45% of the purchase price using debt. So ADC still has plenty of liquidity for additional acquisitions.

Guidance for acquisitions in 2025 is $1.1 to $1.3 billion ($1.2 billion midpoint).

Assuming 25% to 45% is funded through debt, ADC would need $660 to $900 million from issuing equity. They already have about $900 million locked in, so this pipeline is well funded.

Note: ADC typically uses less leverage than most peers. It wouldn’t be surprising if they only fund about 30% with debt. However, commentary on the earnings call implied they might bump leverage a bit higher. Given what they’ve already done with the forward equity offering, a modest bump to leverage would suggest acquisitions above the midpoint of guidance.

Accretion

Shares of ADC are currently $71.50. That is a nice premium to consensus NAV (and I believe consensus NAV figures tend to be inflated for net lease REITs) and over a 16.5x multiple on forward AFFO.

That combination implies ADC’s WACC (weighted average cost of capital) is low enough that the acquisitions should be accretive. This lower can make acquisitions more accretive and it can help ADC bid for better properties. During the quarter the weighted average cap rate for acquisitions was 7.3% and the leases on those properties had a weighted-average remaining term of 12.3 years. That’s a bit lower than we expect from peers, but the higher valuation of ADC’s shares enables it to work well.

Dispositions

We typically expect dispositions to be pretty low.

Guidance for dispositions in 2025 is $10 to $50 million. ($30 million midpoint). This is basically a rounding error.

Once again, ADC is looking good on the fundamentals.

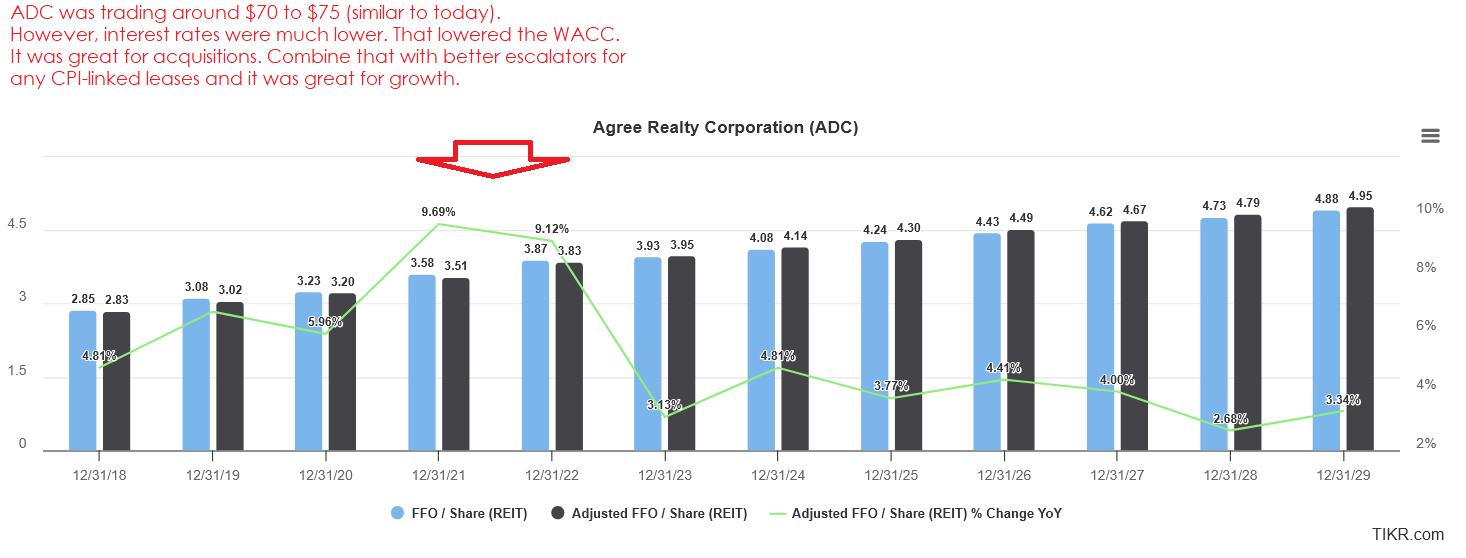

Historical Stability

One last point for ADC is the historical AFFO growth rate. When I reference net lease REITs rarely providing surprises, I think this chart does a great job of demonstrating:

ADC’s growth rate generally fell in a pretty steady range. There were a couple years where it jumped higher, but for the most part the growth is remarkably steady. So why does it tend to be lower now than it was in some of the earlier years? Well, one of the factors is simply that the cost of debt is higher. Acquisitions are still accretive, but they may be slightly less accretive. Over time some debts will also be refinanced to higher rates. That combination holds the growth rate a bit lower. However, the business model continues to work quite well. Investors get a steady dividend that is thoroughly covered by AFFO and a reasonable growth rate.

Historical Correlation

Just one more note here. Sometimes net lease REITs correlate strongly with Treasury yields. Sometimes the correlation completely disappears. Frankly, it’s a bit absurd how the market swings back and forth. It probably merits an updated article on the correlation. When you look at the charts, it’s hard to believe just how strong the correlation is in some periods and how absent the correlation can be during other periods.

Implications for Targets

Much like W.P. Carey (WPC), we’re seeing a similar projected change.

- Impact of fundamentals: Around +2% to +3%.

- Impact of interest rates: around -3% to -8%.

- Combined expected net adjustment: -1% to -5%.

Note: WPC and ADC are reporting similar projected growth rates. However, we believe WPC is getting a slight boost from lease termination fees while ADC is simply continuing to be ADC. Further, management indicates they might be a bit on the conservative side depending on acquisitions. Accretive acquisitions boost the growth rate for current year and next year since they are typically executed throughout the year. Therefore, I’m inclined to think ADC will grow AFFO per share faster than WPC if we do a combined two-year growth rate from 2024 to 2026.

The only challenge with ADC is that the valuation is less favorable than some peers. That’s part of why it’s easier for ADC to create accretion through acquisitions. It’s a nice perk for long-term shareholders, but it makes the price less favorable today.

At $71.50, ADC is currently within our neutral range. Given the projected adjustments, ADC will probably be around the upper end of our neutral range.

Conclusion

Solid quarter for ADC. Nothing shocking, but nothing to dislike. Just all around a good job. The only material headwind for the REIT is coming from interest rates and they continue to navigate the environment well. The impact of higher rates will weigh on all targets, but that’s beyond the control of any REIT.

Disclosure: Long Realty Income (O). No position in WPC or ADC.

Member discussion